Descriptive statistics and inferential statistics are both important components of statistics when learning about a population.

Learning Objective

Contrast descriptive and inferential statistics

Key Points

Descriptive statistics are distinguished from inferential statistics in that descriptive statistics aim to summarize a sample, rather than use the data to learn about the population that the sample of data is thought to represent.

Descriptive statistics provides simple summaries about the sample. These summaries may either form the basis of the initial description of the data as part of a more extensive statistical analysis, or they may be sufficient in and of themselves for a particular investigation.

Statistical inference makes propositions about populations, using data drawn from the population of interest via some form of random sampling. This involves hypothesis testing using a variety of statistical tests.

Key Terms

descriptive statistics

A branch of mathematics dealing with summarization and description of collections of data sets, including the concepts of arithmetic mean, median, and mode.

inferential statistics

A branch of mathematics that involves drawing conclusions about a population based on sample data drawn from it.

Descriptive Statistics vs. Inferential Statistics

Descriptive statistics is the discipline of quantitatively describing the main features of a collection of data, or the quantitative description itself. Descriptive statistics are distinguished from inferential statistics in that descriptive statistics aim to summarize a sample, rather than use the data to learn about the population that the sample of data is thought to represent. This generally means that descriptive statistics, unlike inferential statistics, are not developed on the basis of probability theory. Even when a data analysis draws its main conclusions using inferential statistics, descriptive statistics are generally also presented. For example, in a paper reporting on a study involving human subjects, there typically appears a table giving the overall sample size, sample sizes in important subgroups (e.g., for each treatment or exposure group), and demographic or clinical characteristics such as the average age and the proportion of subjects of each sex.

Descriptive Statistics

Descriptive statistics provides simple summaries about the sample and about the observations that have been made. Such summaries may be either quantitative, i.e. summary statistics, or visual, i.e. simple-to-understand graphs. These summaries may either form the basis of the initial description of the data as part of a more extensive statistical analysis, or they may be sufficient in and of themselves for a particular investigation.

For example, the shooting percentage in basketball is a descriptive statistic that summarizes the performance of a player or a team. This number is the number of shots made divided by the number of shots taken. For example, a player who shoots 33% is making approximately one shot in every three. The percentage summarizes or describes multiple discrete events. Consider also the grade point average. This single number describes the general performance of a student across the range of their course experiences.

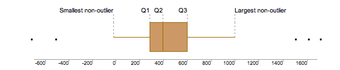

The use of descriptive and summary statistics has an extensive history and, indeed, the simple tabulation of populations and of economic data was the first way the topic of statistics appeared. More recently, a collection of summary techniques has been formulated under the heading of exploratory data analysis: an example of such a technique is the box plot .

Box Plot

The box plot is a graphical depiction of descriptive statistics.

In the business world, descriptive statistics provide a useful summary of security returns when researchers perform empirical and analytical analysis, as they give a historical account of return behavior.

Inferential Statistics

For the most part, statistical inference makes propositions about populations, using data drawn from the population of interest via some form of random sampling. More generally, data about a random process is obtained from its observed behavior during a finite period of time. Given a parameter or hypothesis about which one wishes to make inference, statistical inference most often uses a statistical model of the random process that is supposed to generate the data and a particular realization of the random process.

The conclusion of a statistical inference is a statistical proposition. Some common forms of statistical proposition are:

an estimate; i.e., a particular value that best approximates some parameter of interest

a confidence interval (or set estimate); i.e., an interval constructed using a data set drawn from a population so that, under repeated sampling of such data sets, such intervals would contain the true parameter value with the probability at the stated confidence level

a credible interval; i.e., a set of values containing, for example, 95% of posterior belief

rejection of a hypothesis

clustering or classification of data points into groups

14.1.2: Hypothesis Tests or Confidence Intervals?

Hypothesis tests and confidence intervals are related, but have some important differences.

Learning Objective

Explain how confidence intervals are used to estimate parameters of interest

Key Points

When we conduct a hypothesis test, we assume we know the true parameters of interest.

When we use confidence intervals, we are estimating the the parameters of interest.

The confidence interval for a parameter is not the same as the acceptance region of a test for this parameter, as is sometimes thought.

The confidence interval is part of the parameter space, whereas the acceptance region is part of the sample space.

Key Terms

hypothesis test

A test that defines a procedure that controls the probability of incorrectly deciding that a default position (null hypothesis) is incorrect based on how likely it would be for a set of observations to occur if the null hypothesis were true.

confidence interval

A type of interval estimate of a population parameter used to indicate the reliability of an estimate.

What is the difference between hypothesis testing and confidence intervals? When we conduct a hypothesis test, we assume we know the true parameters of interest. When we use confidence intervals, we are estimating the parameters of interest.

Explanation of the Difference

Confidence intervals are closely related to statistical significance testing. For example, if for some estimated parameter

one wants to test the null hypothesis that

against the alternative that

, then this test can be performed by determining whether the confidence interval for

contains

.

More generally, given the availability of a hypothesis testing procedure that can test the null hypothesis

against the alternative that

for any value of

, then a confidence interval with confidence level

can be defined as containing any number

for which the corresponding null hypothesis is not rejected at significance level

.

In consequence, if the estimates of two parameters (for example, the mean values of a variable in two independent groups of objects) have confidence intervals at a given

value that do not overlap, then the difference between the two values is significant at the corresponding value of

. However, this test is too conservative. If two confidence intervals overlap, the difference between the two means still may be significantly different.

While the formulations of the notions of confidence intervals and of statistical hypothesis testing are distinct, in some senses and they are related, and are complementary to some extent. While not all confidence intervals are constructed in this way, one general purpose approach is to define a

% confidence interval to consist of all those values

for which a test of the hypothesis

is not rejected at a significance level of

%. Such an approach may not always be an option, since it presupposes the practical availability of an appropriate significance test. Naturally, any assumptions required for the significance test would carry over to the confidence intervals.

It may be convenient to say that parameter values within a confidence interval are equivalent to those values that would not be rejected by a hypothesis test, but this would be dangerous. In many instances the confidence intervals that are quoted are only approximately valid, perhaps derived from “plus or minus twice the standard error,” and the implications of this for the supposedly corresponding hypothesis tests are usually unknown.

It is worth noting that the confidence interval for a parameter is not the same as the acceptance region of a test for this parameter, as is sometimes assumed. The confidence interval is part of the parameter space, whereas the acceptance region is part of the sample space. For the same reason, the confidence level is not the same as the complementary probability of the level of significance.

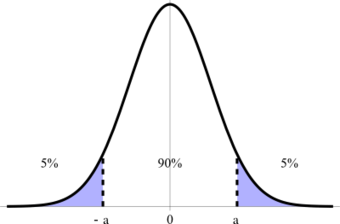

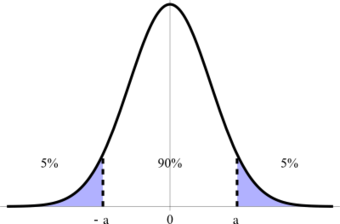

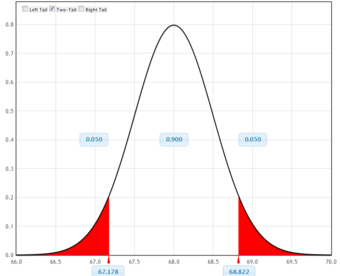

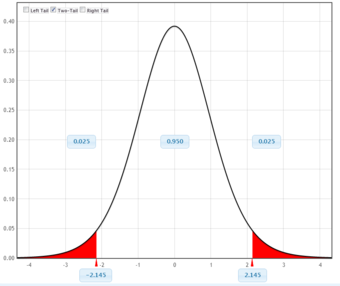

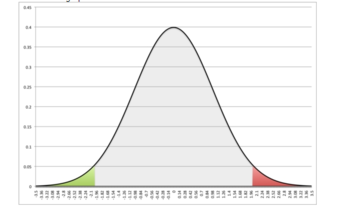

Confidence Interval

This graph illustrates a 90% confidence interval on a standard normal curve.

14.1.3: Quantitative or Qualitative Data?

Different statistical tests are used to test quantitative and qualitative data.

Learning Objective

Contrast quantitative and qualitative data

Key Points

Quantitative (numerical) data is any data that is in numerical form, such as statistics and percentages.

Qualitative (categorical) data deals with descriptions with words, such as gender or nationality.

Paired and unpaired t-tests and z-tests are just some of the statistical tests that can be used to test quantitative data.

One of the most common statistical tests for qualitative data is the chi-square test (both the goodness of fit test and test of independence).

Key Terms

central limit theorem

The theorem that states: If the sum of independent identically distributed random variables has a finite variance, then it will be (approximately) normally distributed.

quantitative

of a measurement based on some quantity or number rather than on some quality

qualitative

of descriptions or distinctions based on some quality rather than on some quantity

Quantitative Data vs. Qualitative Data

Recall the differences between quantitative and qualitative data.

Quantitative (numerical) data is any data that is in numerical form, such as statistics, percentages, et cetera. In layman’s terms, a researcher studying quantitative data asks a specific, narrow question and collects a sample of numerical data from participants to answer the question. The researcher analyzes the data with the help of statistics and hopes the numbers will yield an unbiased result that can be generalized to some larger population.

Qualitative (categorical) research, on the other hand, asks broad questions and collects word data from participants. The researcher looks for themes and describes the information in themes and patterns exclusive to that set of participants. Examples of qualitative variables are male/female, nationality, color, et cetera.

Quantitative Data Tests

Paired and unpaired t-tests and z-tests are just some of the statistical tests that can be used to test quantitative data. We will give a brief overview of these tests here.

A t-test is any statistical hypothesis test in which the test statistic follows a t distribution if the null hypothesis is supported. It can be used to determine if two sets of data are significantly different from each other and is most commonly applied when the test statistic would follow a normal distribution if the value of a scaling term in the test statistic were known. When the scaling term is unknown and is replaced by an estimate based on the data, the test statistic (under certain conditions) follows a t distribution .

t Distribution

Plots of the t distribution for several different degrees of freedom.

A z-test is any statistical test for which the distribution of the test statistic under the null hypothesis can be approximated by a normal distribution. Because of the central limit theorem, many test statistics are approximately normally distributed for large samples. For each significance level, the z-test has a single critical value. This fact makes it more convenient than the t-test, which has separate critical values for each sample size. Therefore, many statistical tests can be conveniently performed as approximate z-tests if the sample size is large or the population variance known.

Qualitative Data Tests

One of the most common statistical tests for qualitative data is the chi-square test (both the goodness of fit test and test of independence).

The chi-square test tests a null hypothesis stating that the frequency distribution of certain events observed in a sample is consistent with a particular theoretical distribution. The events considered must be mutually exclusive and have total probability. A common case for this test is where the events each cover an outcome of a categorical variable. A test of goodness of fit establishes whether or not an observed frequency distribution differs from a theoretical distribution, and a test of independence assesses whether paired observations on two variables, expressed in a contingency table, are independent of each other (e.g., polling responses from people of different nationalities to see if one’s nationality is related to the response).

14.1.4: One, Two, or More Groups?

Different statistical tests are required when there are different numbers of groups (or samples).

Learning Objective

Identify the appropriate statistical test required for a group of samples

Key Points

One-sample tests are appropriate when a sample is being compared to the population from a hypothesis. The population characteristics are known from theory or are calculated from the population.

Two-sample tests are appropriate for comparing two samples, typically experimental and control samples from a scientifically controlled experiment.

Paired tests are appropriate for comparing two samples where it is impossible to control important variables.

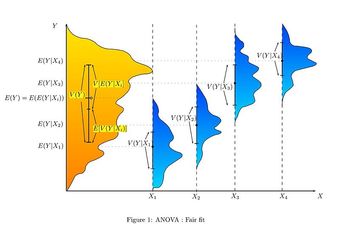

-tests (analysis of variance, also called ANOVA) are used when there are more than two groups. They are commonly used when deciding whether groupings of data by category are meaningful.

Key Terms

z-test

Any statistical test for which the distribution of the test statistic under the null hypothesis can be approximated by a normal distribution.

t-test

Any statistical hypothesis test in which the test statistic follows a Student’s $t$-distribution if the null hypothesis is supported.

Depending on how many groups (or samples) with which we are working, different statistical tests are required.

One-sample tests are appropriate when a sample is being compared to the population from a hypothesis. The population characteristics are known from theory, or are calculated from the population. Two-sample tests are appropriate for comparing two samples, typically experimental and control samples from a scientifically controlled experiment. Paired tests are appropriate for comparing two samples where it is impossible to control important variables. Rather than comparing two sets, members are paired between samples so the difference between the members becomes the sample. Typically the mean of the differences is then compared to zero.

The number of groups or samples is also an important deciding factor when determining which test statistic is appropriate for a particular hypothesis test. A test statistic is considered to be a numerical summary of a data-set that reduces the data to one value that can be used to perform a hypothesis test. Examples of test statistics include the

-statistic,

-statistic, chi-square statistic, and

-statistic.

A

-statistic may be used for comparing one or two samples or proportions. When comparing two proportions, it is necessary to use a pooled standard deviation for the

-test. The formula to calculate a

-statistic for use in a one-sample

-test is as follows:

where

is the sample mean,

is the population mean,

is the population standard deviation, and

is the sample size.

A

-statistic may be used for one sample, two samples (with a pooled or unpooled standard deviation), or for a regression

-test. The formula to calculate a

-statistic for a one-sample

-test is as follows:

where

is the sample mean,

is the population mean,

is the sample standard deviation, and

is the sample size.

-tests (analysis of variance, also called ANOVA) are used when there are more than two groups. They are commonly used when deciding whether groupings of data by category are meaningful. If the variance of test scores of the left-handed in a class is much smaller than the variance of the whole class, then it may be useful to study lefties as a group. The null hypothesis is that two variances are the same, so the proposed grouping is not meaningful.

14.2: A Closer Look at Tests of Significance

14.2.1: Was the Result Significant?

Results are deemed significant if they are found to have occurred by some reason other than chance.

Learning Objective

Assess the statistical significance of data for a null hypothesis

Key Points

In statistical testing, a result is deemed statistically significant if it is so extreme (without external variables which would influence the correlation results of the test) that such a result would be expected to arise simply by chance only in rare circumstances.

If a test of significance gives a p-value lower than or equal to the significance level, the null hypothesis is rejected at that level.

Different levels of cutoff trade off countervailing effects. Lower levels – such as 0.01 instead of 0.05 – are stricter, and increase confidence in the determination of significance, but run an increased risk of failing to reject a false null hypothesis.

Key Terms

statistical significance

A measure of how unlikely it is that a result has occurred by chance.

null hypothesis

A hypothesis set up to be refuted in order to support an alternative hypothesis; presumed true until statistical evidence in the form of a hypothesis test indicates otherwise.

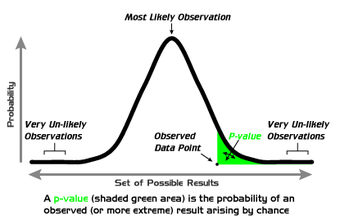

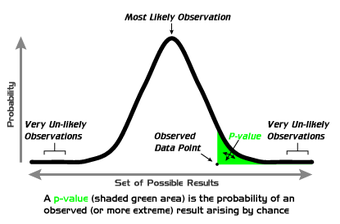

Statistical significance refers to two separate notions: the p-value (the probability that the observed data would occur by chance in a given single null hypothesis); or the Type I error rate α (false positive rate) of a statistical hypothesis test (the probability of incorrectly rejecting a given null hypothesis in favor of a second alternative hypothesis).

A fixed number, most often 0.05, is referred to as a significance level or level of significance; such a number may be used either in the first sense, as a cutoff mark for p-values (each p-value is calculated from the data), or in the second sense as a desired parameter in the test design (α depends only on the test design, and is not calculated from observed data). In this atom, we will focus on the p-value notion of significance.

What is Statistical Significance?

Statistical significance is a statistical assessment of whether observations reflect a pattern rather than just chance. When used in statistics, the word significant does not mean important or meaningful, as it does in everyday speech; with sufficient data, a statistically significant result may be very small in magnitude.

The fundamental challenge is that any partial picture of a given hypothesis, poll, or question is subject to random error. In statistical testing, a result is deemed statistically significant if it is so extreme (without external variables which would influence the correlation results of the test) that such a result would be expected to arise simply by chance only in rare circumstances. Hence the result provides enough evidence to reject the hypothesis of ‘no effect’.

For example, tossing 3 coins and obtaining 3 heads would not be considered an extreme result. However, tossing 10 coins and finding that all 10 land the same way up would be considered an extreme result: for fair coins, the probability of having the first coin matched by all 9 others is rare. The result may therefore be considered statistically significant evidence that the coins are not fair.

The calculated statistical significance of a result is in principle only valid if the hypothesis was specified before any data were examined. If, instead, the hypothesis was specified after some of the data were examined, and specifically tuned to match the direction in which the early data appeared to point, the calculation would overestimate statistical significance.

Use in Practice

Popular levels of significance are 10% (0.1), 5% (0.05), 1% (0.01), 0.5% (0.005), and 0.1% (0.001). If a test of significance gives a p-value lower than or equal to the significance level , the null hypothesis is rejected at that level. Such results are informally referred to as ‘statistically significant (at the p = 0.05 level, etc.)’. For example, if someone argues that “there’s only one chance in a thousand this could have happened by coincidence”, a 0.001 level of statistical significance is being stated. The lower the significance level chosen, the stronger the evidence required. The choice of significance level is somewhat arbitrary, but for many applications, a level of 5% is chosen by convention.

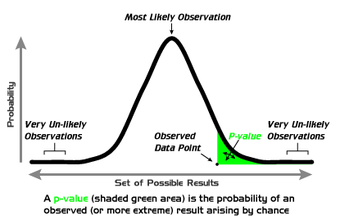

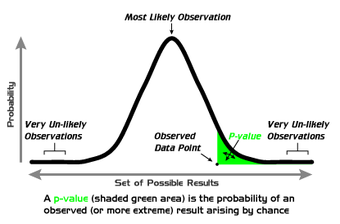

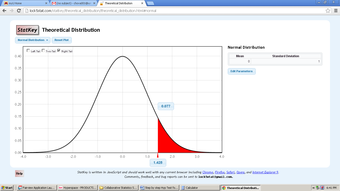

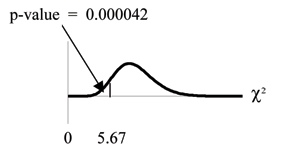

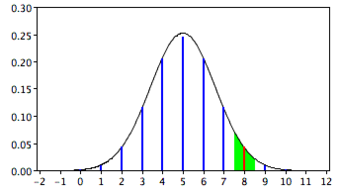

P-Values

A graphical depiction of the meaning of p-values.

Different levels of cutoff trade off countervailing effects. Lower levels – such as 0.01 instead of 0.05 – are stricter, and increase confidence in the determination of significance, but run an increased risk of failing to reject a false null hypothesis. Evaluation of a given p-value of data requires a degree of judgment, and rather than a strict cutoff, one may instead simply consider lower p-values as more significant.

14.2.2: Data Snooping: Testing Hypotheses Once You’ve Seen the Data

Testing hypothesis once you’ve seen the data may result in inaccurate conclusions.

Learning Objective

Explain how to test a hypothesis using data

Key Points

Testing a hypothesis suggested by the data can very easily result in false positives (type I errors). If one looks long enough and in enough different places, eventually data can be found to support any hypothesis.

If the hypothesis was specified after some of the data were examined, and specifically tuned to match the direction in which the early data appeared to point, the calculation would overestimate statistical significance.

Sometimes, people deliberately test hypotheses once they’ve seen the data. Data snooping (also called data fishing or data dredging) is the inappropriate (sometimes deliberately so) use of data mining to uncover misleading relationships in data.

Key Terms

Type I error

Rejecting the null hypothesis when the null hypothesis is true.

data snooping

the inappropriate (sometimes deliberately so) use of data mining to uncover misleading relationships in data

The calculated statistical significance of a result is in principle only valid if the hypothesis was specified before any data were examined. If, instead, the hypothesis was specified after some of the data were examined, and specifically tuned to match the direction in which the early data appeared to point, the calculation would overestimate statistical significance.

Testing Hypotheses Suggested by the Data

Testing a hypothesis suggested by the data can very easily result in false positives (type I errors) . If one looks long enough and in enough different places, eventually data can be found to support any hypothesis. Unfortunately, these positive data do not by themselves constitute evidence that the hypothesis is correct. The negative test data that were thrown out are just as important, because they give one an idea of how common the positive results are compared to chance. Running an experiment, seeing a pattern in the data, proposing a hypothesis from that pattern, then using the same experimental data as evidence for the new hypothesis is extremely suspect, because data from all other experiments, completed or potential, has essentially been “thrown out” by choosing to look only at the experiments that suggested the new hypothesis in the first place.

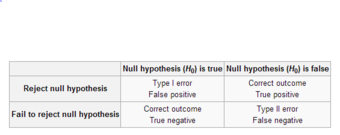

Types of Errors

This table depicts the difference types of errors in significance testing.

A large set of tests as described above greatly inflates the probability of type I error as all but the data most favorable to the hypothesis is discarded. This is a risk, not only in hypothesis testing but in all statistical inference as it is often problematic to accurately describe the process that has been followed in searching and discarding data. In other words, one wants to keep all data (regardless of whether they tend to support or refute the hypothesis) from “good tests”, but it is sometimes difficult to figure out what a “good test” is. It is a particular problem in statistical modelling, where many different models are rejected by trial and error before publishing a result.

The error is particularly prevalent in data mining and machine learning. It also commonly occurs in academic publishing where only reports of positive, rather than negative, results tend to be accepted, resulting in the effect known as publication bias..

Data Snooping

Sometimes, people deliberately test hypotheses once they’ve seen the data. Data snooping (also called data fishing or data dredging) is the inappropriate (sometimes deliberately so) use of data mining to uncover misleading relationships in data. Data-snooping bias is a form of statistical bias that arises from this misuse of statistics. Any relationships found might appear valid within the test set but they would have no statistical significance in the wider population. Although data-snooping bias can occur in any field that uses data mining, it is of particular concern in finance and medical research, which both heavily use data mining.

14.2.3: Was the Result Important?

The results are deemed important if they change the effects of an event.

Learning Objective

Distinguish the difference between the terms ‘significance’ and ‘importance’ in statistical assessments

Key Points

When used in statistics, the word significant does not mean important or meaningful, as it does in everyday speech; with sufficient data, a statistically significant result may be very small in magnitude.

Importance is a measure of the effects of the event. A difference can be significant, but not important.

It is preferable for researchers to not look solely at significance, but to examine effect-size statistics, which describe how large the effect is and the uncertainty around that estimate, so that the practical importance of the effect may be gauged by the reader.

Key Terms

null hypothesis

A hypothesis set up to be refuted in order to support an alternative hypothesis; presumed true until statistical evidence in the form of a hypothesis test indicates otherwise.

statistical significance

A measure of how unlikely it is that a result has occurred by chance.

Significance vs. Importance

Statistical significance is a statistical assessment of whether observations reflect a pattern rather than just chance. When used in statistics, the word significant does not mean important or meaningful, as it does in everyday speech; with sufficient data, a statistically significant result may be very small in magnitude.

If a test of significance gives a

-value lower than or equal to the significance level, the null hypothesis is rejected at that level . Such results are informally referred to as ‘statistically significant (at the

level, etc.)’. For example, if someone argues that “there’s only one chance in a thousand this could have happened by coincidence”, a

level of statistical significance is being stated. Once again, this does not mean that the findings are important.

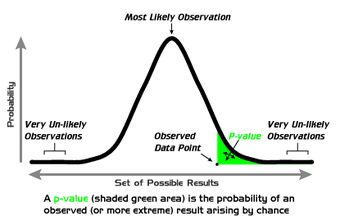

-Values

A graphical depiction of the meaning of

-values.

So what is importance? Importance is a measure of the effects of the event. For example, we could measure two different one-cup measuring cups enough times to find that their volumes are statistically different at a significance level of

. But is this difference important? Would this slight difference make a difference in the cookies you’re trying to bake? No. The difference in this case is statistically significant at a certain level, but not important.

Researchers focusing solely on whether individual test results are significant or not may miss important response patterns which individually fall under the threshold set for tests of significance. Therefore along with tests of significance, it is preferable to examine effect-size statistics, which describe how large the effect is and the uncertainty around that estimate, so that the practical importance of the effect may be gauged by the reader.

14.2.4: The Role of the Model

A statistical model is a set of assumptions concerning the generation of the observed data and similar data.

Learning Objective

Explain the significance of valid models in statistical inference

Key Points

Statisticians distinguish between three levels of modeling assumptions: fully-parametric, non-parametric, and semi-parametric.

Descriptions of statistical models usually emphasize the role of population quantities of interest, about which we wish to draw inference. Descriptive statistics are typically used as a preliminary step before more formal inferences are drawn.

Whatever level of assumption is made, correctly calibrated inference in general requires these assumptions to be correct; i.e., that the data-generating mechanisms have been correctly specified.

Key Terms

Simple Random Sampling

Method where each individual is chosen randomly and entirely by chance, such that each individual has the same probability of being chosen at any stage during the sampling process, and each subset of k individuals has the same probability of being chosen for the sample as any other subset of k individuals.

covariate

a variable that is possibly predictive of the outcome under study

Any statistical inference requires assumptions. A statistical model is a set of assumptions concerning the generation of the observed data and similar data. Descriptions of statistical models usually emphasize the role of population quantities of interest, about which we wish to draw inference. Descriptive statistics are typically used as a preliminary step before more formal inferences are drawn.

Degrees of Models

Statisticians distinguish between three levels of modeling assumptions:

Fully-parametric. The probability distributions describing the data-generation process are assumed to be fully described by a family of probability distributions involving only a finite number of unknown parameters. For example, one may assume that the distribution of population values is truly Normal , with unknown mean and variance, and that data sets are generated by simple random sampling. The family of generalized linear models is a widely used and flexible class of parametric models.

Non-parametric. The assumptions made about the process generating the data are much fewer than in parametric statistics and may be minimal. For example, every continuous probability distribution has a median that may be estimated using the sample median, which has good properties when the data arise from simple random sampling.

Semi-parametric. This term typically implies assumptions in between fully and non-parametric approaches. For example, one may assume that a population distribution has a finite mean. Furthermore, one may assume that the mean response level in the population depends in a truly linear manner on some covariate (a parametric assumption), but not make any parametric assumption describing the variance around that mean. More generally, semi-parametric models can often be separated into ‘structural’ and ‘random variation’ components. One component is treated parametrically and the other non-parametrically.

Importance of Valid Models

Whatever level of assumption is made, correctly calibrated inference in general requires these assumptions to be correct (i.e., that the data-generating mechanisms have been correctly specified).

Incorrect assumptions of simple random sampling can invalidate statistical inference. More complex semi- and fully parametric assumptions are also cause for concern. For example, incorrect “Assumptions of Normality” in the population invalidate some forms of regression-based inference. The use of any parametric model is viewed skeptically by most experts in sampling human populations. In particular, a normal distribution would be a totally unrealistic and unwise assumption to make if we were dealing with any kind of economic population. Here, the central limit theorem states that the distribution of the sample mean for very large samples is approximately normally distributed, if the distribution is not heavy tailed.

14.2.5: Does the Difference Prove the Point?

Rejecting the null hypothesis does not necessarily prove the alternative hypothesis.

Learning Objective

Assess whether a null hypothesis should be accepted or rejected

Key Points

The “fail to reject” terminology highlights the fact that the null hypothesis is assumed to be true from the start of the test; therefore, if there is a lack of evidence against it, it simply continues to be assumed true.

The phrase “accept the null hypothesis” may suggest it has been proven simply because it has not been disproved, a logical fallacy known as the argument from ignorance.

Unless a test with particularly high power is used, the idea of “accepting” the null hypothesis may be dangerous.

Whether rejection of the null hypothesis truly justifies acceptance of the alternative hypothesis depends on the structure of the hypotheses.

Hypothesis testing emphasizes the rejection, which is based on a probability, rather than the acceptance, which requires extra steps of logic.

Key Terms

null hypothesis

A hypothesis set up to be refuted in order to support an alternative hypothesis; presumed true until statistical evidence in the form of a hypothesis test indicates otherwise.

p-value

The probability of obtaining a test statistic at least as extreme as the one that was actually observed, assuming that the null hypothesis is true.

alternative hypothesis

a rival hypothesis to the null hypothesis, whose likelihoods are compared by a statistical hypothesis test

In statistical hypothesis testing, tests are used in determining what outcomes of a study would lead to a rejection of the null hypothesis for a pre-specified level of significance; this can help to decide whether results contain enough information to cast doubt on conventional wisdom, given that conventional wisdom has been used to establish the null hypothesis. The critical region of a hypothesis test is the set of all outcomes which cause the null hypothesis to be rejected in favor of the alternative hypothesis.

Accepting the Null Hypothesis vs. Failing to Reject It

It is important to note the philosophical difference between accepting the null hypothesis and simply failing to reject it. The “fail to reject” terminology highlights the fact that the null hypothesis is assumed to be true from the start of the test; if there is a lack of evidence against it, it simply continues to be assumed true. The phrase “accept the null hypothesis” may suggest it has been proved simply because it has not been disproved, a logical fallacy known as the argument from ignorance. Unless a test with particularly high power is used, the idea of “accepting” the null hypothesis may be dangerous. Nonetheless, the terminology is prevalent throughout statistics, where its meaning is well understood.

Alternatively, if the testing procedure forces us to reject the null hypothesis (

), we can accept the alternative hypothesis (

) and we conclude that the research hypothesis is supported by the data. This fact expresses that our procedure is based on probabilistic considerations in the sense we accept that using another set of data could lead us to a different conclusion.

What Does This Mean?

If the

-value is less than the required significance level (equivalently, if the observed test statistic is in the critical region), then we say the null hypothesis is rejected at the given level of significance. Rejection of the null hypothesis is a conclusion. This is like a “guilty” verdict in a criminal trial—the evidence is sufficient to reject innocence, thus proving guilt. We might accept the alternative hypothesis (and the research hypothesis).

-Values

A graphical depiction of the meaning of

-values.

If the

-value is not less than the required significance level (equivalently, if the observed test statistic is outside the critical region), then the test has no result. The evidence is insufficient to support a conclusion. This is like a jury that fails to reach a verdict. The researcher typically gives extra consideration to those cases where the

-value is close to the significance level.

Whether rejection of the null hypothesis truly justifies acceptance of the research hypothesis depends on the structure of the hypotheses. Rejecting the hypothesis that a large paw print originated from a bear does not immediately prove the existence of Bigfoot. The two hypotheses in this case are not exhaustive; there are other possibilities. Maybe a moose made the footprints. Hypothesis testing emphasizes the rejection which is based on a probability rather than the acceptance which requires extra steps of logic.

A t-test is any statistical hypothesis test in which the test statistic follows a Student’s t-distribution if the null hypothesis is supported.

Learning Objective

Outline the appropriate uses of t-tests in Student’s t-distribution

Key Points

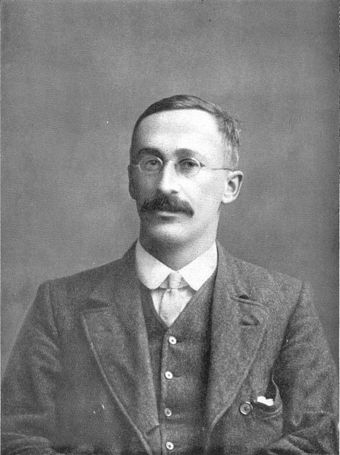

The t-statistic was introduced in 1908 by William Sealy Gosset, a chemist working for the Guinness brewery in Dublin, Ireland.

The t-test can be used to determine if two sets of data are significantly different from each other.

The t-test is most commonly applied when the test statistic would follow a normal distribution if the value of a scaling term in the test statistic were known.

Key Terms

t-test

Any statistical hypothesis test in which the test statistic follows a Student’s t-distribution if the null hypothesis is supported.

Student’s t-distribution

A family of continuous probability distributions that arises when estimating the mean of a normally distributed population in situations where the sample size is small and population standard deviation is unknown.

A t-test is any statistical hypothesis test in which the test statistic follows a Student’s t-distribution if the null hypothesis is supported. It can be used to determine if two sets of data are significantly different from each other, and is most commonly applied when the test statistic would follow a normal distribution if the value of a scaling term in the test statistic were known. When the scaling term is unknown and is replaced by an estimate based on the data, the test statistic (under certain conditions) follows a Student’s t-distribution.

History

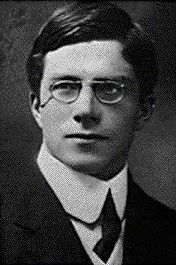

The t-statistic was introduced in 1908 by William Sealy Gosset (shown in ), a chemist working for the Guinness brewery in Dublin, Ireland. Gosset had been hired due to Claude Guinness’s policy of recruiting the best graduates from Oxford and Cambridge to apply biochemistry and statistics to Guinness’s industrial processes. Gosset devised the t-test as a cheap way to monitor the quality of stout. The t-test work was submitted to and accepted in the journal Biometrika, the journal that Karl Pearson had co-founded and for which he served as the Editor-in-Chief. The company allowed Gosset to publish his mathematical work, but only if he used a pseudonym (he chose “Student”). Gosset left Guinness on study-leave during the first two terms of the 1906-1907 academic year to study in Professor Karl Pearson’s Biometric Laboratory at University College London. Gosset’s work on the t-test was published in Biometrika in 1908.

William Sealy Gosset

Writing under the pseudonym “Student”, Gosset published his work on the t-test in 1908.

Uses

Among the most frequently used t-tests are:

A one-sample location test of whether the mean of a normally distributed population has a value specified in a null hypothesis.

A two-sample location test of a null hypothesis that the means of two normally distributed populations are equal. All such tests are usually called Student’s t-tests, though strictly speaking that name should only be used if the variances of the two populations are also assumed to be equal. The form of the test used when this assumption is dropped is sometimes called Welch’s t-test. These tests are often referred to as “unpaired” or “independent samples” t-tests, as they are typically applied when the statistical units underlying the two samples being compared are non-overlapping.

A test of a null hypothesis that the difference between two responses measured on the same statistical unit has a mean value of zero. For example, suppose we measure the size of a cancer patient’s tumor before and after a treatment. If the treatment is effective, we expect the tumor size for many of the patients to be smaller following the treatment. This is often referred to as the “paired” or “repeated measures” t-test.

A test of whether the slope of a regression line differs significantly from 0.

13.1.2: The t-Distribution

Student’s

-distribution arises in estimation problems where the goal is to estimate an unknown parameter when the data are observed with additive errors.

Learning Objective

Calculate the Student’s $t$-distribution

Key Points

Student’s

-distribution (or simply the

-distribution) is a family of continuous probability distributions that arises when estimating the mean of a normally distributed population in situations where the sample size is small and population standard deviation is unknown.

The

-distribution (for

) can be defined as the distribution of the location of the true mean, relative to the sample mean and divided by the sample standard deviation, after multiplying by the normalizing term.

The

-distribution with

degrees of freedom is the sampling distribution of the

-value when the samples consist of independent identically distributed observations from a normally distributed population.

As the number of degrees of freedom grows, the

-distribution approaches the normal distribution with mean

and variance

.

Key Terms

confidence interval

A type of interval estimate of a population parameter used to indicate the reliability of an estimate.

Student’s t-distribution

A family of continuous probability distributions that arises when estimating the mean of a normally distributed population in situations where the sample size is small and population standard deviation is unknown.

chi-squared distribution

A distribution with $k$ degrees of freedom is the distribution of a sum of the squares of $k$ independent standard normal random variables.

Student’s

-distribution (or simply the

-distribution) is a family of continuous probability distributions that arises when estimating the mean of a normally distributed population in situations where the sample size is small and population standard deviation is unknown. It plays a role in a number of widely used statistical analyses, including the Student’s

-test for assessing the statistical significance of the difference between two sample means, the construction of confidence intervals for the difference between two population means, and in linear regression analysis.

If we take

samples from a normal distribution with fixed unknown mean and variance, and if we compute the sample mean and sample variance for these

samples, then the

-distribution (for

) can be defined as the distribution of the location of the true mean, relative to the sample mean and divided by the sample standard deviation, after multiplying by the normalizing term

, where

is the sample size. In this way, the

-distribution can be used to estimate how likely it is that the true mean lies in any given range.

The

-distribution with

degrees of freedom is the sampling distribution of the

-value when the samples consist of independent identically distributed observations from a normally distributed population. Thus, for inference purposes,

is a useful “pivotal quantity” in the case when the mean and variance (

,

) are unknown population parameters, in the sense that the

-value has then a probability distribution that depends on neither

nor

.

History

The

-distribution was first derived as a posterior distribution in 1876 by Helmert and Lüroth. In the English-language literature it takes its name from William Sealy Gosset’s 1908 paper in Biometrika under the pseudonym “Student.” Gosset worked at the Guinness Brewery in Dublin, Ireland, and was interested in the problems of small samples, for example of the chemical properties of barley where sample sizes might be as small as three participants. Gosset’s paper refers to the distribution as the “frequency distribution of standard deviations of samples drawn from a normal population.” It became well known through the work of Ronald A. Fisher, who called the distribution “Student’s distribution” and referred to the value as

.

Distribution of a Test Statistic

Student’s

-distribution with

degrees of freedom can be defined as the distribution of the random variable

:

where:

is normally distributed with expected value

and variance

V has a chi-squared distribution with

degrees of freedom

and

are independent

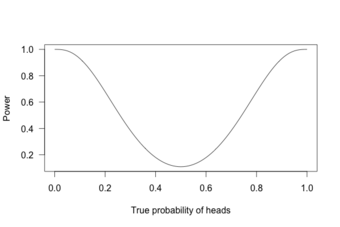

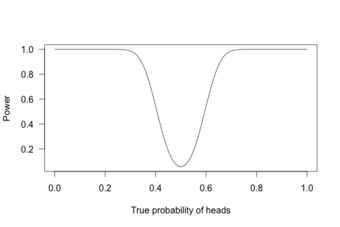

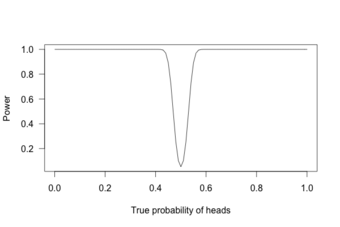

A different distribution is defined as that of the random variable defined, for a given constant

, by:

This random variable has a noncentral

-distribution with noncentrality parameter

. This distribution is important in studies of the power of Student’s

-test.

Shape

The probability density function is symmetric; its overall shape resembles the bell shape of a normally distributed variable with mean

and variance

, except that it is a bit lower and wider. In more technical terms, it has heavier tails, meaning that it is more prone to producing values that fall far from its mean. This makes it useful for understanding the statistical behavior of certain types of ratios of random quantities, in which variation in the denominator is amplified and may produce outlying values when the denominator of the ratio falls close to zero. As the number of degrees of freedom grows, the

-distribution approaches the normal distribution with mean

and variance

.

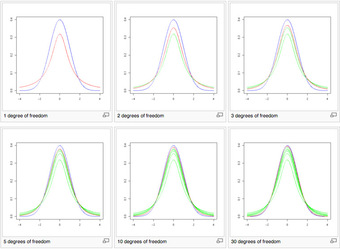

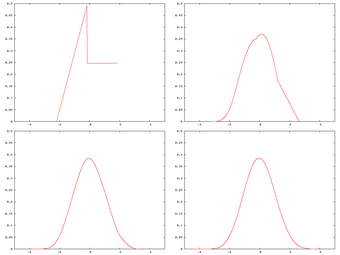

Shape of the

-Distribution

These images show the density of the

-distribution (red) for increasing values of

(1, 2, 3, 5, 10, and 30 degrees of freedom). The normal distribution is shown as a blue line for comparison. Previous plots are shown in green. Note that the

-distribution becomes closer to the normal distribution as

increases.

Uses

Student’s

-distribution arises in a variety of statistical estimation problems where the goal is to estimate an unknown parameter, such as a mean value, in a setting where the data are observed with additive errors. If (as in nearly all practical statistical work) the population standard deviation of these errors is unknown and has to be estimated from the data, the

-distribution is often used to account for the extra uncertainty that results from this estimation. In most such problems, if the standard deviation of the errors were known, a normal distribution would be used instead of the

-distribution.

Confidence intervals and hypothesis tests are two statistical procedures in which the quantiles of the sampling distribution of a particular statistic (e.g., the standard score) are required. In any situation where this statistic is a linear function of the data, divided by the usual estimate of the standard deviation, the resulting quantity can be rescaled and centered to follow Student’s

-distribution. Statistical analyses involving means, weighted means, and regression coefficients all lead to statistics having this form.

A number of statistics can be shown to have

-distributions for samples of moderate size under null hypotheses that are of interest, so that the

-distribution forms the basis for significance tests. For example, the distribution of Spearman’s rank correlation coefficient

, in the null case (zero correlation) is well approximated by the

-distribution for sample sizes above about

.

13.1.3: Assumptions

Assumptions of a

-test depend on the population being studied and on how the data are sampled.

Learning Objective

Explain the underlying assumptions of a $t$-test

Key Points

Most

-test statistics have the form

, where

and

are functions of the data.

Typically,

is designed to be sensitive to the alternative hypothesis (i.e., its magnitude tends to be larger when the alternative hypothesis is true), whereas

is a scaling parameter that allows the distribution of

to be determined.

The assumptions underlying a

-test are that:

follows a standard normal distribution under the null hypothesis, and

follows a

distribution with

degrees of freedom under the null hypothesis, where

is a positive constant.

and

are independent.

Key Terms

scaling parameter

A special kind of numerical parameter of a parametric family of probability distributions; the larger the scale parameter, the more spread out the distribution.

alternative hypothesis

a rival hypothesis to the null hypothesis, whose likelihoods are compared by a statistical hypothesis test

t-test

Any statistical hypothesis test in which the test statistic follows a Student’s $t$-distribution if the null hypothesis is supported.

Most

-test statistics have the form

, where

and

are functions of the data. Typically,

is designed to be sensitive to the alternative hypothesis (i.e., its magnitude tends to be larger when the alternative hypothesis is true), whereas

is a scaling parameter that allows the distribution of

to be determined.

As an example, in the one-sample

-test:

where

is the sample mean of the data,

is the sample size, and

is the population standard deviation of the data;

in the one-sample

-test is

, where

is the sample standard deviation.

The assumptions underlying a

-test are that:

follows a standard normal distribution under the null hypothesis.

follows a

distribution with

degrees of freedom under the null hypothesis, where

is a positive constant.

and

are independent.

In a specific type of

-test, these conditions are consequences of the population being studied, and of the way in which the data are sampled. For example, in the

-test comparing the means of two independent samples, the following assumptions should be met:

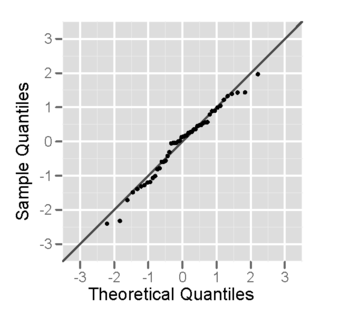

Each of the two populations being compared should follow a normal distribution. This can be tested using a normality test, or it can be assessed graphically using a normal quantile plot.

If using Student’s original definition of the

-test, the two populations being compared should have the same variance (testable using the

-test or assessable graphically using a Q-Q plot). If the sample sizes in the two groups being compared are equal, Student’s original

-test is highly robust to the presence of unequal variances. Welch’s

-test is insensitive to equality of the variances regardless of whether the sample sizes are similar.

The data used to carry out the test should be sampled independently from the two populations being compared. This is, in general, not testable from the data, but if the data are known to be dependently sampled (i.e., if they were sampled in clusters), then the classical

-tests discussed here may give misleading results.

13.1.4: t-Test for One Sample

The

-test is the most powerful parametric test for calculating the significance of a small sample mean.

Learning Objective

Derive the degrees of freedom for a t-test

Key Points

A one sample

-test has the null hypothesis, or

, of

.

The

-test is the small-sample analog of the

test, which is suitable for large samples.

For a

-test the degrees of freedom of the single mean is

because only one population parameter (the population mean) is being estimated by a sample statistic (the sample mean).

Key Terms

t-test

Any statistical hypothesis test in which the test statistic follows a Student’s $t$-distribution if the null hypothesis is supported.

degrees of freedom

any unrestricted variable in a frequency distribution

The

-test is the most powerful parametric test for calculating the significance of a small sample mean. A one sample

-test has the null hypothesis, or

, that the population mean equals the hypothesized value. Expressed formally:

where the Greek letter

represents the population mean and

represents its assumed (hypothesized) value. The

-test is the small sample analog of the

-test, which is suitable for large samples. A small sample is generally regarded as one of size

.

In order to perform a

-test, one first has to calculate the degrees of freedom. This quantity takes into account the sample size and the number of parameters that are being estimated. Here, the population parameter

is being estimated by the sample statistic

, the mean of the sample data. For a

-test the degrees of freedom of the single mean is

. This is because only one population parameter (the population mean) is being estimated by a sample statistic (the sample mean).

Example

A college professor wants to compare her students’ scores with the national average. She chooses a simple random sample of

students who score an average of

on a standardized test. Their scores have a standard deviation of

. The national average on the test is a

. She wants to know if her students scored significantly lower than the national average.

1. First, state the problem in terms of a distribution and identify the parameters of interest. Mention the sample. We will assume that the scores (

) of the students in the professor’s class are approximately normally distributed with unknown parameters

and

.

2. State the hypotheses in symbols and words:

i.e.: The null hypothesis is that her students scored on par with the national average.

i.e.: The alternative hypothesis is that her students scored lower than the national average.

3. Identify the appropriate test to use. Since we have a simple random sample of small size and do not know the standard deviation of the population, we will use a one-sample

-test. The formula for the

-statistic

for a one-sample test is as follows:

,

where

is the sample mean and

is the sample standard deviation. The standard deviation of the sample divided by the square root of the sample size is known as the “standard error” of the sample.

4. State the distribution of the test statistic under the null hypothesis. Under

the statistic

will follow a Student’s distribution with

degrees of freedom:

.

5. Compute the observed value

of the test statistic

, by entering the values, as follows:

6. Determine the so-called

-value of the value

of the test statistic

. We will reject the null hypothesis for too-small values of

, so we compute the left

-value:

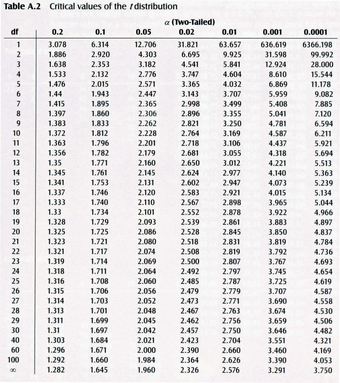

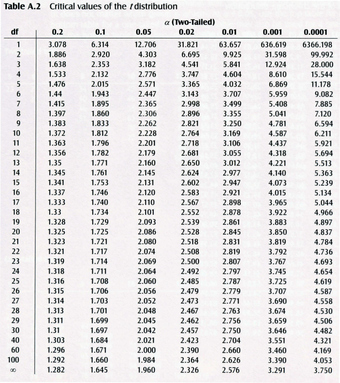

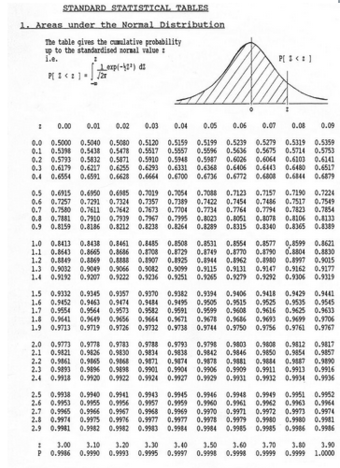

The Student’s distribution gives

at probabilities

and degrees of freedom

. The

-value is approximated at

.

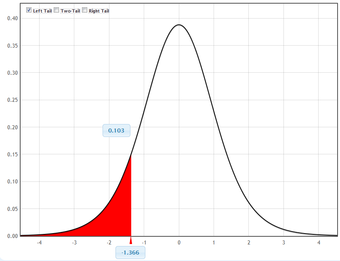

7. Lastly, interpret the results in the context of the problem. The

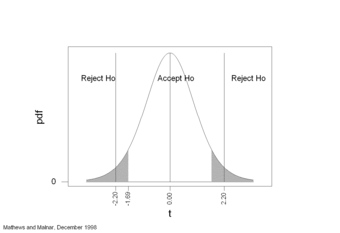

-value indicates that the results almost certainly did not happen by chance and we have sufficient evidence to reject the null hypothesis. This is to say, the professor’s students did score significantly lower than the national average.

13.1.5: t-Test for Two Samples: Independent and Overlapping

Two-sample t-tests for a difference in mean involve independent samples, paired samples, and overlapping samples.

Learning Objective

Contrast paired and unpaired samples in a two-sample t-test

Key Points

For the null hypothesis, the observed t-statistic is equal to the difference between the two sample means divided by the standard error of the difference between the sample means.

The independent samples t-test is used when two separate sets of independent and identically distributed samples are obtained—one from each of the two populations being compared.

An overlapping samples t-test is used when there are paired samples with data missing in one or the other samples.

Key Terms

blocking

A schedule for conducting treatment combinations in an experimental study such that any effects on the experimental results due to a known change in raw materials, operators, machines, etc., become concentrated in the levels of the blocking variable.

null hypothesis

A hypothesis set up to be refuted in order to support an alternative hypothesis; presumed true until statistical evidence in the form of a hypothesis test indicates otherwise.

The two sample t-test is used to compare the means of two independent samples. For the null hypothesis, the observed t-statistic is equal to the difference between the two sample means divided by the standard error of the difference between the sample means. If the two population variances can be assumed equal, the standard error of the difference is estimated from the weighted variance about the means. If the variances cannot be assumed equal, then the standard error of the difference between means is taken as the square root of the sum of the individual variances divided by their sample size. In the latter case the estimated t-statistic must either be tested with modified degrees of freedom, or it can be tested against different critical values. A weighted t-test must be used if the unit of analysis comprises percentages or means based on different sample sizes.

The two-sample t-test is probably the most widely used (and misused) statistical test. Comparing means based on convenience sampling or non-random allocation is meaningless. If, for any reason, one is forced to use haphazard rather than probability sampling, then every effort must be made to minimize selection bias.

Unpaired and Overlapping Two-Sample T-Tests

Two-sample t-tests for a difference in mean involve independent samples, paired samples and overlapping samples. Paired t-tests are a form of blocking, and have greater power than unpaired tests when the paired units are similar with respect to “noise factors” that are independent of membership in the two groups being compared. In a different context, paired t-tests can be used to reduce the effects of confounding factors in an observational study.

Independent Samples

The independent samples t-test is used when two separate sets of independent and identically distributed samples are obtained, one from each of the two populations being compared. For example, suppose we are evaluating the effect of a medical treatment, and we enroll 100 subjects into our study, then randomize 50 subjects to the treatment group and 50 subjects to the control group. In this case, we have two independent samples and would use the unpaired form of the t-test .

Medical Treatment Research

Medical experimentation may utilize any two independent samples t-test.

Overlapping Samples

An overlapping samples t-test is used when there are paired samples with data missing in one or the other samples (e.g., due to selection of “I don’t know” options in questionnaires, or because respondents are randomly assigned to a subset question). These tests are widely used in commercial survey research (e.g., by polling companies) and are available in many standard crosstab software packages.

13.1.6: t-Test for Two Samples: Paired

Paired-samples

-tests typically consist of a sample of matched pairs of similar units, or one group of units that has been tested twice.

Learning Objective

Criticize the shortcomings of paired-samples $t$-tests

Key Points

A paired-difference test uses additional information about the sample that is not present in an ordinary unpaired testing situation, either to increase the statistical power or to reduce the effects of confounders.

-tests are carried out as paired difference tests for normally distributed differences where the population standard deviation of the differences is not known.

A paired samples

-test based on a “matched-pairs sample” results from an unpaired sample that is subsequently used to form a paired sample, by using additional variables that were measured along with the variable of interest.

Paired samples

-tests are often referred to as “dependent samples

-tests” (as are

-tests on overlapping samples).

Key Terms

paired difference test

A type of location test that is used when comparing two sets of measurements to assess whether their population means differ.

confounding

Describes a phenomenon in which an extraneous variable in a statistical model correlates (positively or negatively) with both the dependent variable and the independent variable; confounder = noun form.

Paired Difference Test

In statistics, a paired difference test is a type of location test used when comparing two sets of measurements to assess whether their population means differ. A paired difference test uses additional information about the sample that is not present in an ordinary unpaired testing situation, either to increase the statistical power or to reduce the effects of confounders.

-tests are carried out as paired difference tests for normally distributed differences where the population standard deviation of the differences is not known.

Paired-Samples

-Test

Paired samples

-tests typically consist of a sample of matched pairs of similar units, or one group of units that has been tested twice (a “repeated measures”

-test).

A typical example of the repeated measures t-test would be where subjects are tested prior to a treatment, say for high blood pressure, and the same subjects are tested again after treatment with a blood-pressure lowering medication . By comparing the same patient’s numbers before and after treatment, we are effectively using each patient as their own control. That way the correct rejection of the null hypothesis (here: of no difference made by the treatment) can become much more likely, with statistical power increasing simply because the random between-patient variation has now been eliminated.

Blood Pressure Treatment

A typical example of a repeated measures

-test is in the treatment of patients with high blood pressure to determine the effectiveness of a particular medication.

Note, however, that an increase of statistical power comes at a price: more tests are required, each subject having to be tested twice. Because half of the sample now depends on the other half, the paired version of Student’s

-test has only

degrees of freedom (with

being the total number of observations. Pairs become individual test units, and the sample has to be doubled to achieve the same number of degrees of freedom.

A paired-samples

-test based on a “matched-pairs sample” results from an unpaired sample that is subsequently used to form a paired sample, by using additional variables that were measured along with the variable of interest. The matching is carried out by identifying pairs of values consisting of one observation from each of the two samples, where the pair is similar in terms of other measured variables. This approach is sometimes used in observational studies to reduce or eliminate the effects of confounding factors.

Paired-samples

-tests are often referred to as “dependent samples

-tests” (as are

-tests on overlapping samples).

13.1.7: Calculations for the t-Test: One Sample

The following is a discussion on explicit expressions that can be used to carry out various

-tests.

Learning Objective

Assess a null hypothesis in a one-sample $t$-test

Key Points

In each case, the formula for a test statistic that either exactly follows or closely approximates a

-distribution under the null hypothesis is given.

Also, the appropriate degrees of freedom are given in each case.

Once a

-value is determined, a

-value can be found using a table of values from Student’s

-distribution.

If the calculated

-value is below the threshold chosen for statistical significance (usually the

, the

, or

level), then the null hypothesis is rejected in favor of the alternative hypothesis.

Key Terms

standard error

A measure of how spread out data values are around the mean, defined as the square root of the variance.

p-value

The probability of obtaining a test statistic at least as extreme as the one that was actually observed, assuming that the null hypothesis is true.

The following is a discussion on explicit expressions that can be used to carry out various

-tests. In each case, the formula for a test statistic that either exactly follows or closely approximates a

-distribution under the null hypothesis is given. Also, the appropriate degrees of freedom are given in each case. Each of these statistics can be used to carry out either a one-tailed test or a two-tailed test.

Once a

-value is determined, a

-value can be found using a table of values from Student’s

-distribution. If the calculated

-value is below the threshold chosen for statistical significance (usually the

, the

, or

level), then the null hypothesis is rejected in favor of the alternative hypothesis.

One-Sample T-Test

In testing the null hypothesis that the population mean is equal to a specified value

, one uses the statistic:

where

is the sample mean,

is the sample standard deviation of the sample and

is the sample size. The degrees of freedom used in this test is

.

Slope of a Regression

Suppose one is fitting the model:

where

are known,

and

are unknown, and

are independent identically normally distributed random errors with expected value

and unknown variance

, and

are observed. It is desired to test the null hypothesis that the slope

is equal to some specified value

(often taken to be

, in which case the hypothesis is that

and

are unrelated). Let

and

be least-squares estimators, and let

and

, respectively, be the standard errors of those least-squares estimators. Then,

has a

-distribution with

degrees of freedom if the null hypothesis is true. The standard error of the slope coefficient is:

can be written in terms of the residuals

:

Therefore, the sum of the squares of residuals, or

, is given by:

Then, the

-score is given by:

13.1.8: Calculations for the t-Test: Two Samples

The following is a discussion on explicit expressions that can be used to carry out various t-tests.

Learning Objective

Calculate the t value for different types of sample sizes and variances in an independent two-sample t-test

Key Points

A two-sample t-test for equal sample sizes and equal variances is only used when both the two sample sizes are equal and it can be assumed that the two distributions have the same variance.

A two-sample t-test for unequal sample sizes and equal variances is used only when it can be assumed that the two distributions have the same variance.

A two-sample t-test for unequal (or equal) sample sizes and unequal variances (also known as Welch’s t-test) is used only when the two population variances are assumed to be different and hence must be estimated separately.

Key Terms

pooled variance

A method for estimating variance given several different samples taken in different circumstances where the mean may vary between samples but the true variance is assumed to remain the same.

degrees of freedom

any unrestricted variable in a frequency distribution

The following is a discussion on explicit expressions that can be used to carry out various t-tests. In each case, the formula for a test statistic that either exactly follows or closely approximates a t-distribution under the null hypothesis is given. Also, the appropriate degrees of freedom are given in each case. Each of these statistics can be used to carry out either a one-tailed test or a two-tailed test.

Once a t-value is determined, a p-value can be found using a table of values from Student’s t-distribution. If the calculated p-value is below the threshold chosen for statistical significance (usually the 0.10, the 0.05, or 0.01 level), then the null hypothesis is rejected in favor of the alternative hypothesis.

Independent Two-Sample T-Test

Equal Sample Sizes, Equal Variance

This test is only used when both:

the two sample sizes (that is, the number, n, of participants of each group) are equal; and

it can be assumed that the two distributions have the same variance.

Violations of these assumptions are discussed below. The t-statistic to test whether the means are different can be calculated as follows:

,

where

.

Here,

is the grand standard deviation (or pooled standard deviation), 1 = group one, 2 = group two. The denominator of t is the standard error of the difference between two means.

For significance testing, the degrees of freedom for this test is 2n − 2 where n is the number of participants in each group.

Unequal Sample Sizes, Equal Variance

This test is used only when it can be assumed that the two distributions have the same variance. The t-statistic to test whether the means are different can be calculated as follows:

,

where .

Pooled Variance

This is the formula for a pooled variance in a two-sample t-test with unequal sample size but equal variances.

is an estimator of the common standard deviation of the two samples: it is defined in this way so that its square is an unbiased estimator of the common variance whether or not the population means are the same. In these formulae, n = number of participants, 1 = group one, 2 = group two. n − 1 is the number of degrees of freedom for either group, and the total sample size minus two (that is, n1 + n2 − 2) is the total number of degrees of freedom, which is used in significance testing.

This test, also known as Welch’s t-test, is used only when the two population variances are assumed to be different (the two sample sizes may or may not be equal) and hence must be estimated separately. The t-statistic to test whether the population means are different is calculated as:

where .

Unpooled Variance

This is the formula for a pooled variance in a two-sample t-test with unequal or equal sample sizes but unequal variances.

Here s2 is the unbiased estimator of the variance of the two samples, ni = number of participants in group i, i=1 or 2. Note that in this case

is not a pooled variance. For use in significance testing, the distribution of the test statistic is approximated as an ordinary Student’s t-distribution with the degrees of freedom calculated using:

.

Welch–Satterthwaite Equation

This is the formula for calculating the degrees of freedom in Welsh’s t-test.

This is known as the Welch–Satterthwaite equation. The true distribution of the test statistic actually depends (slightly) on the two unknown population variances.

13.1.9: Multivariate Testing

Hotelling’s

-square statistic allows for the testing of hypotheses on multiple (often correlated) measures within the same sample.

Learning Objective

Summarize Hotelling’s $T$-squared statistics for one- and two-sample multivariate tests

Key Points

Hotelling’s

-squared distribution is important because it arises as the distribution of a set of statistics which are natural generalizations of the statistics underlying Student’s

-distribution.

In particular, the distribution arises in multivariate statistics in undertaking tests of the differences between the (multivariate) means of different populations, where tests for univariate problems would make use of a

-test.

For a one-sample multivariate test, the hypothesis is that the mean vector (

) is equal to a given vector (

).

For a two-sample multivariate test, the hypothesis is that the mean vectors (

and

) of two samples are equal.

Key Terms

Hotelling’s T-square statistic

A generalization of Student’s $t$-statistic that is used in multivariate hypothesis testing.

Type I error

An error occurring when the null hypothesis ($H_0$) is true, but is rejected.

A generalization of Student’s

-statistic, called Hotelling’s

-square statistic, allows for the testing of hypotheses on multiple (often correlated) measures within the same sample. For instance, a researcher might submit a number of subjects to a personality test consisting of multiple personality scales (e.g., the Minnesota Multiphasic Personality Inventory). Because measures of this type are usually highly correlated, it is not advisable to conduct separate univariate

-tests to test hypotheses, as these would neglect the covariance among measures and inflate the chance of falsely rejecting at least one hypothesis (type I error). In this case a single multivariate test is preferable for hypothesis testing. Hotelling’s

statistic follows a

distribution.

Hotelling’s

-squared distribution is important because it arises as the distribution of a set of statistics which are natural generalizations of the statistics underlying Student’s

-distribution. In particular, the distribution arises in multivariate statistics in undertaking tests of the differences between the (multivariate) means of different populations, where tests for univariate problems would make use of a

-test. It is proportional to the

-distribution.

One-sample

Test

For a one-sample multivariate test, the hypothesis is that the mean vector (

) is equal to a given vector (

). The test statistic is defined as follows:

where

is the sample size,

is the vector of column means and

is a

sample covariance matrix.

Two-Sample T2 Test

For a two-sample multivariate test, the hypothesis is that the mean vectors (

) of two samples are equal. The test statistic is defined as:

13.1.10: Alternatives to the t-Test

When the normality assumption does not hold, a nonparametric alternative to the

-test can often have better statistical power.

Learning Objective

Explain how Wilcoxon Rank Sum tests are applied to data distributions

Key Points

The

-test provides an exact test for the equality of the means of two normal populations with unknown, but equal, variances.

The Welch’s

-test is a nearly exact test for the case where the data are normal but the variances may differ.

For moderately large samples and a one-tailed test, the

is relatively robust to moderate violations of the normality assumption.

If the sample size is large, Slutsky’s theorem implies that the distribution of the sample variance has little effect on the distribution of the test statistic.

For two independent samples when the data distributions are asymmetric (that is, the distributions are skewed) or the distributions have large tails, then the Wilcoxon Rank Sum test can have three to four times higher power than the

-test.

The nonparametric counterpart to the paired-samples

-test is the Wilcoxon signed-rank test for paired samples.

Key Terms

central limit theorem

The theorem that states: If the sum of independent identically distributed random variables has a finite variance, then it will be (approximately) normally distributed.

Wilcoxon Rank Sum test

A non-parametric test of the null hypothesis that two populations are the same against an alternative hypothesis, especially that a particular population tends to have larger values than the other.

Wilcoxon signed-rank test

A nonparametric statistical hypothesis test used when comparing two related samples, matched samples, or repeated measurements on a single sample to assess whether their population mean ranks differ (i.e., it is a paired difference test).

The

-test provides an exact test for the equality of the means of two normal populations with unknown, but equal, variances. The Welch’s

-test is a nearly exact test for the case where the data are normal but the variances may differ. For moderately large samples and a one-tailed test, the

is relatively robust to moderate violations of the normality assumption.