4.1: The Drive for International Trade

4.1.1: Competitive Advantage

Competitive advantage is defined as the strategic advantage one business entity has over its rival entities within its competitive industry.

Learning Objective

Differentiate between the theories of competitive advantage and comparative advantage

Key Points

- A country is said to have a comparative advantage in the production of a good (say cloth) if it can produce cloth at a lower opportunity cost than another country.

- Competitive advantage seeks to address some of the criticisms of comparative advantage.

- Competitive advantage occurs when an organization acquires or develops an attribute or combination of attributes that allows it to outperform its competitors.

Key Terms

- comparative advantage

-

The concept that a certain good can be produced more efficiently than others due to a number of factors, including productive skills, climate, natural resource availability, and so forth.

- Opportunity cost

-

The cost of an opportunity forgone (and the loss of the benefits that could be received from that opportunity); the most valuable forgone alternative.

Example

- Opportunity cost – The opportunity cost of cloth production is defined as the amount of wine for example, that must be given up in order to produce one more unit of cloth.

Competitive advantage is defined as the strategic advantage one business entity has over its rival entities within its competitive industry. Achieving competitive advantage strengthens and positions a business better within the business environment.

Competitive advantage seeks to address some of the criticisms of comparative advantage. A country is said to have a comparative advantage in the production of a good (say cloth) if it can produce cloth at a lower opportunity cost than another country. The opportunity cost of cloth production is defined as the amount of wine that must be given up in order to produce one more unit of cloth. Thus, England would have the comparative advantage in cloth production relative to Portugal if it must give up less wine to produce another unit of cloth than the amount of wine that Portugal would have to give up to produce another unit of cloth.

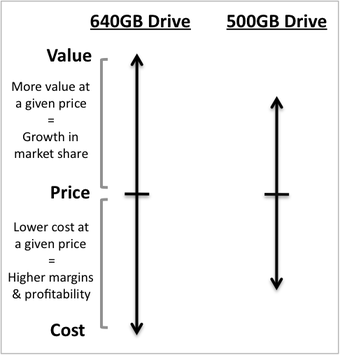

Competitive Advantage

The 640GB drive has a competitive advantage over the 500GB drive in terms of both cost and value.

Michael Porter proposed the theory of competitive advantage in 1985. The competitive advantage theory suggests that states and businesses should pursue policies that create high-quality goods to sell at high prices in the market. Porter emphasizes productivity growth as the focus of national strategies. This theory rests on the notion that cheap labor is ubiquitous, and natural resources are not necessary for a good economy. The other theory, comparative advantage, can lead countries to specialize in exporting primary goods and raw materials that trap countries in low-wage economies due to terms of trade. The competitive advantage theory attempts to correct for this issue by stressing maximizing scale economies in goods and services that garner premium prices.

Competitive advantage occurs when an organization acquires or develops an attribute or combination of attributes that allows it to outperform its competitors. These attributes can include access to natural resources, such as high grade ores or inexpensive power or access to highly trained and skilled personnel human resources. New technologies, such as robotics and information technology, are either to be included as a part of the product or to assist making it. Information technology has become such a prominent part of the modern business world that it can also contribute to competitive advantage by outperforming competitors with regard to Internet presence. From the very beginning (i.e., Adam Smith’s Wealth of Nations), the central problem of information transmittal, leading to the rise of middle men in the marketplace, has been a significant impediment in gaining competitive advantage. By using the Internet as the middle man, the purveyor of information to the final consumer, businesses can gain a competitive advantage through creation of an effective website, which in the past required extensive effort finding the right middle man and cultivating the relationship.

4.1.2: Absolute Advantage and the Balance of Trade

Absolute advantage and balance of trade are two important aspects of international trade that affect countries and organizations.

Learning Objective

Explain the principles of absolute advantage and balance of trade

Key Points

- Absolute advantage: In economics, the principle of absolute advantage refers to the ability of a party (an individual, or firm, or country) to produce more of a good or service than competitors, using the same amount of resources.

- Net exports: The balance of trade (or net exports, sometimes symbolized as NX) is the difference between the monetary value of exports and imports of output in an economy over a certain period. It is the relationship between a nation’s imports and exports.

- Advantageous trade is based on comparative advantage and covers a larger set of circumstances while still including the case of absolute advantage and hence is a more general theory.

Key Terms

- Absolute advantage

-

The capability to produce more of a given product using less of a given resource than a competing entity.

- advantageous

-

Being of advantage; conferring advantage; gainful; profitable; useful; beneficial; as, an advantageous position.

In the drive for international trade, it is important to understand how trade affects countries positively and negatively—both how a country’s imports and exports affect its economy and how effectively the country’s ability to create and export vital goods effects the businesses within that country. Absolute advantage and balance of trade are two important aspects of international trade that affect countries and organizations .

European Free Trade Agreement

The European Free Trade Agreement has helped countries trade internationally without worrying about absolute advantage and increased net exports.

Absolute Advantage

In economics, the principle of absolute advantage refers to the ability of a party (an individual, a firm, or a country) to produce more of a good or service than competitors while using the same amount of resources. Adam Smith first described the principle of absolute advantage in the context of international trade, using labor as the only input. Since absolute advantage is determined by a simple comparison of labor productivities, it is possible for a party to have no absolute advantage in anything; in that case, according to the theory of absolute advantage, no trade will occur with the other party. It can be contrasted with the concept of comparative advantage, which refers to the ability to produce a particular good at a lower opportunity cost.

Balance of Trade

The balance of trade (or net exports, sometimes symbolized as NX) is the difference between the monetary value of exports and imports in an economy over a certain period. A positive balance is known as a trade surplus if it consists of exporting more than is imported; a negative balance is referred to as a trade deficit or, informally, a trade gap. The balance of trade is sometimes divided into a goods and a services balance.

4.1.3: Importing and Exporting

Nations export products for which they have a competitive advantage in order to import products for which they lack a competitive advantage.

Learning Objective

Explain the difference between imports and exports

Key Points

- Exports refers to selling goods and services produced in the home country to other markets.

- Imports are derived from the conceptual meaning, as to bringing in the goods and services into the port of a country.

- An import in the receiving country is an export to the sending country.

Key Term

- capital goods

-

Produced goods that are chiefly used in production of further goods, in contrast to the consumer goods

In International Trade, “exports” refers to selling goods and services produced in the home country to other markets. Any good or commodity, transported from one country to another country in a legitimate fashion, typically for use in trade. Export goods or services are provided to foreign consumers by domestic producers. The buyer of such goods and services is referred to an “importer” who is based in the country of import, whereas the overseas-based seller is referred to as an “exporter. ” Thus, an import is any good (e.g., a commodity) or service brought in from one country to another country in a legitimate fashion, typically for use in trade. It is a good that is brought in from another country for sale. Import goods or services are provided to domestic consumers by foreign producers. An import in the receiving country is an export to the sending country.

When a country, South Africa for example, sells its products to other countries, we call it exporting, and when South Africa buys goods from other countries, we call it importing. South Africa exports mainly primary products, such as products from mining (gold, diamonds, platinum, manganese, chromium, coal, iron ore, and asbestos), and agricultural products, such as wool, sugar, hides, and fruit. South Africa purchases capital goods, such as machinery, computers, and electronic products, from other countries. The money that is earned through exports is used to pay for imported products and in this way, the numerous needs of South Africans are satisfied.

Container Ship in Kaoshiung Habor, ROC

Exporting raw materials accounts for the funds spent on importing finished goods.

4.2: International Trade Barriers

4.2.1: Economics

Trade barriers are government-induced restrictions on international trade, which generally decrease overall economic efficiency.

Learning Objective

Explain the different types of trade barriers and their economic effect

Key Points

- Trade barriers cause a limited choice of products and, therefore, would force customers to pay higher prices and accept inferior quality.

- Trade barriers generally favor rich countries because these countries tend to set international trade policies and standards.

- Economists generally agree that trade barriers are detrimental and decrease overall economic efficiency, which can be explained by the theory of comparative advantage.

Key Terms

- tariff

-

A system of government-imposed duties levied on imported or exported goods; a list of such duties, or the duties themselves.

- quota

-

a restriction on the import of something to a specific quantity.

Trade barriers are government-induced restrictions on international trade. Man-made trade barriers come in several forms, including:

- Tariffs

- Non-tariff barriers to trade

- Import licenses

- Export licenses

- Import quotas

- Subsidies

- Voluntary Export Restraints

- Local content requirements

- Embargo

- Currency devaluation

- Trade restriction

Most trade barriers work on the same principle–the imposition of some sort of cost on trade that raises the price of the traded products. If two or more nations repeatedly use trade barriers against each other, then a trade war results.

A port in Singapore

International trade barriers can take many forms for any number of reasons. Generally, governments impose barriers to protect domestic industry or to “punish” a trading partner.

Economists generally agree that trade barriers are detrimental and decrease overall economic efficiency. This can be explained by the theory of comparative advantage. In theory, free trade involves the removal of all such barriers, except perhaps those considered necessary for health or national security. In practice, however, even those countries promoting free trade heavily subsidize certain industries, such as agriculture and steel. Trade barriers are often criticized for the effect they have on the developing world. Because rich-country players set trade policies, goods, such as agricultural products that developing countries are best at producing, face high barriers. Trade barriers, such as taxes on food imports or subsidies for farmers in developed economies, lead to overproduction and dumping on world markets, thus lowering prices and hurting poor-country farmers. Tariffs also tend to be anti-poor, with low rates for raw commodities and high rates for labor-intensive processed goods. The Commitment to Development Index measures the effect that rich country trade policies actually have on the developing world. Another negative aspect of trade barriers is that it would cause a limited choice of products and, therefore, would force customers to pay higher prices and accept inferior quality.

In general, for a given level of protection, quota-like restrictions carry a greater potential for reducing welfare than do tariffs. Tariffs, quotas, and non-tariff barriers lead too few of the economy’s resources being used to produce tradeable goods. An export subsidy can also be used to give an advantage to a domestic producer over a foreign producer. Export subsidies tend to have a particularly strong negative effect because in addition to distorting resource allocation, they reduce the economy’s terms of trade. In contrast to tariffs, export subsidies lead to an over allocation of the economy’s resources to the production of tradeable goods.

4.2.2: Ethical Barriers

Despite international trading laws and declarations, countries continue to face challenges around ethical trading and business practices.

Learning Objective

Explain how and why groups place ethical barriers on international trade

Key Points

- Although some argue that the increasing integration of financial markets between countries leads to more consistent and seamless trading practices, others point out that capital flows tend to favor the capital owners more than any other group.

- With increased international trade and global capital flows, critics argue that income disparities between the rich and poor are exacerbated, and industrialized nations grow in power at the expense of under-capitalized countries.

- Anti-globalization groups continue to protest what they view as the unethical trading practices of multinational businesses and capitalist nations, often targeting groups such as the WTO and IMF.

Key Terms

- neoliberalism

-

A political movement that espouses economic liberalism as a means of promoting economic development and securing political liberty.

- GDP

-

Gross Domestic Product (Economics). A measure of the economic production of a particular territory in financial capital terms over a specific time period.

Ethical Barriers

International trade is the exchange of goods and services across national borders. In most countries, it represents a significant part of gross domestic product (GDP). The rise of industrialization, globalization, and technological innovation has increased the importance of international trade, as well as its economic, social, and political effects on the countries involved. Internationally recognized ethical practices such as the UN Global Compact have been instituted to facilitate mutual cooperation and benefit between governments, businesses, and public institutions. Nevertheless, countries continue to face challenges around ethical trading and business practices, especially regarding economic inequalities and human rights violations.

Arguments Against International Trade

Capital markets involve the raising and investing money in various enterprises. Although some argue that the increasing integration of these financial markets between countries leads to more consistent and seamless trading practices, others point out that capital flows tend to favor the capital owners more than any other group. Likewise, owners and workers in specific sectors in capital-exporting countries bear much of the burden of adjusting to increased movement of capital. The economic strains and eventual hardships that result from these conditions lead to political divisions about whether or not to encourage or increase integration of international trade markets. Moreover, critics argue that income disparities between the rich and poor are exacerbated, and industrialized nations grow in power at the expense of under-capitalized countries.

Anti-Globalization Movements

The anti-globalization movement is a worldwide activist movement that is critical of the globalization of capitalism. Anti-globalization activists are particularly critical of the undemocratic nature of capitalist globalization and the promotion of neoliberalism by international institutions such as the International Monetary Fund (IMF) and the World Bank. Other common targets of anti-corporate and anti-globalization movements include the Organisation for Economic Co-operation and Development (OECD), the WTO, and free trade treaties like the North American Free Trade Agreement (NAFTA), Free Trade Area of the Americas (FTAA), the Multilateral Agreement on Investment (MAI), and the General Agreement on Trade in Services (GATS). Meetings of such bodies are often met with strong protests, as demonstrators attempt to bring attention to the often devastating effects of global capital on local conditions.

On November 30, 1999, close to fifty thousand people gathered to protest the WTO meetings in Seattle, Washington. Labor, economic, and environmental activists succeeded in disrupting and closing the meetings due to their disapproval of corporate globalization. This event came to symbolize the increased debate and growing conflict around the ethical questions on international trade, globalization and capitalization .

Criticism of the Global Capitalist Economy

Demonstrations, such as the mass protest at the 1999 WTO meeting in Seattle, highlight ethical questions on the effects of international trade on poor and developing nations.

4.2.3: Cultural Barriers

It is typically more difficult to do business in a foreign country than in one’s home country due to cultural barriers.

Learning Objective

Explain how cultural differences can pose as barriers to international business

Key Points

- With the process of globalization and increasing global trade, it is unavoidable that different cultures will meet, conflict, and blend together. People from different cultures find it is hard to communicate not only due to language barriers but also cultural differences.

- It is typically more difficult to do business in a foreign country than in one’s home country, especially in the early stages when a firm is considering either physical investment in or product expansion to another country.

- Expansion planning requires an in-depth knowledge of existing market channels and suppliers, of consumer preferences and current purchase behavior, and of domestic and foreign rules and regulations.

- Recognize useful strategic frameworks and tools for assessing variance in cultural predisposition, such as Hofstede’s Cultural Dimensions Theory.

Key Terms

- red tape

-

A derisive term for regulations or bureaucratic procedures that are considered excessive or excessively time- and effort-consuming.

- individualism

-

The tendency for a person to act without reference to others, particularly in matters of style, fashion or mode of thought.

Culture and Global Business

It is typically more difficult to do business in a foreign country than in one’s home country, especially in the early stages when a firm is considering either physical investment in or product expansion to another country. Expansion planning requires an in-depth knowledge of existing market channels and suppliers, of consumer preferences and current purchase behavior, and of domestic and foreign rules and regulations. Language and cultural barriers present considerable challenges, as well as institutional differences among countries.

With the process of globalization and increasing global trade, it is unavoidable that different cultures will meet, conflict, and blend together. People from different cultures find it hard to communicate not only due to language barriers but also because of cultural differences.

In a survey of Texas agricultural exporting firms, Hollon (1989) found that from a firm management perspective, the initial entry into export markets was significantly more difficult than either the handling of ongoing export activities or the consideration of expansion to new export product lines or markets. From a list of 38 items in three categories (knowledge gaps, marketing aspects, and financial aspects) over three time horizons (start-up, ongoing, and expansion), the three problems rated most difficult were all start-up phase marketing items:

- Poor knowledge of emerging markets or lack of information on potentially profitable markets

- Foreign market entry problems and overseas product promotion and distribution

- Complexity of the export transaction, including documentation and “red tape.”

Two of these items, market entry and transaction complexity, remained problematic in ongoing operations and in new product market expansion. Import restrictions and export competition became more problematic in later phases, while financial problems were pervasive at all phases of the export operation.

Tools for Understanding Cultural Deviations in Business

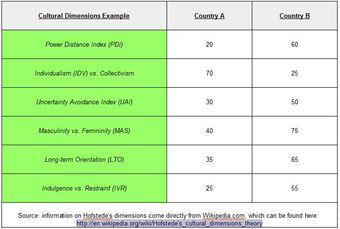

Recognizing that different geographic regions and/or nationalities represent vastly different business operating characteristics, often due to differences in cultural predisposition, is a critical building block for successful global business leaders. As a result, various researchers in global business have generated business models to illustrate key cultural considerations between different countries. The most recognized and utilized in the field is Geert Hofstede’s Cultural Dimensions Theory, which encompasses six cultural deviations highly relevant to business managers. The figure below provides an example of this model:

Hofstede’s Cultural Dimensions Theory Example

As you can see in the above figure, the six dimensions underline differences in perspective in each category. Two countries (or more) are selected for comparison, at which point can identify differences in business practices based on cultural barriers. For example, Country A demonstrates lower power distance compared to Country B. This means that a resident of Country A operating in Country B must understand that lines of authority are more rigid in Country B and act accordingly.

To briefly explain each dimension:

- PDI rating represents a stronger acceptance of authority in a given culture

- IDV (individualism) rating indicates the degree to which individuals are focused upon as opposed to the broader group

- UAI represents the degree to which risk-taking is commonplace (a higher rating meaning a lower propensity for risk)

- MAS represents the scale between competitiveness, materialism and aggressiveness (high rating) compared to focusing on relationships and quality of life

- LTO indicates the tendency to plan for longer-term agenda items as opposed to pursuing short-term goals

- IVR is simply the frugal (or spendthrift) habits of the average individual in a culture (purchasing beyond necessity)

4.2.4: Technological Barriers

Standards-related trade measures, known in WTO parlance as technical barriers to trade play a critical role in shaping global trade.

Learning Objective

Explain how technical standards can be barriers to trade

Key Points

- Governments, market participants, and other entities can use standards-related measures as an effective and efficient means of achieving legitimate commercial and policy objectives.

- Significant foreign trade barriers in the form of product standards, technical regulations and testing, certification, and other procedures are involved in determining whether or not products conform to standards and technical regulations.

Key Terms

- enterprise

-

A company, business, organization, or other purposeful endeavor.

- standard

-

A level of quality or attainment.

U.S. companies, farmers, ranchers, and manufacturers increasingly encounter non-tariff trade barriers in the form of product standards, testing requirements, and other technical requirements as they seek to sell products and services around the world. As tariff barriers to industrial and agricultural trade have fallen, standards-related measures of this kind have emerged as a key concern. Governments, market participants, and other entities can use standards-related measures as an effective and efficient means of achieving legitimate commercial and policy objectives. But when standards-related measures are outdated, overly burdensome, discriminatory, or otherwise inappropriate, these measures can reduce competition, stifle innovation, and create unnecessary technical barriers to trade. These kinds of measures can pose a particular problem for small- and medium-sized enterprises (SMEs), which often do not have the resources to address these problems on their own. Significant foreign trade barriers in the form of product standards, technical regulations and testing, certification, and other procedures are involved in determining whether or not products conform to standards and technical regulations.

These standards-related trade measures, known in World Trade Organization (WTO) parlance as “technical barriers to trade,” play a critical role in shaping the flow of global trade. Standards-related measures serve an important function in facilitating global trade, including by enabling greater access to international markets by SMEs. Standards-related measures also enable governments to pursue legitimate objectives, such as protecting human health and the environment and preventing deceptive practices. But standards-related measures that are non-transparent, discriminatory, or otherwise unwarranted can act as significant barriers to U.S. trade. These kinds of measures can pose a particular problem for SMEs, which often do not have the resources to address these problems on their own.

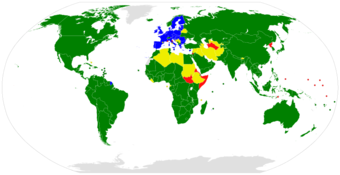

Members of the World Trade Organization

Most countries are now part of the World Trade Organization. Those that are not are concentrated in northeast Africa, Oceania, and the Middle East. The European Union is its own bloc within the W.T.O.

4.2.5: The Argument for Barriers

Some argue that imports from countries with low wages has put downward pressure on the wages of Americans and therefore we should have trade barriers.

Learning Objective

Argue in support of trade barriers

Key Points

- Economy-wide trade creates jobs in industries that have a comparative advantage and destroys jobs in industries that have a comparative disadvantage.

- Trade barriers protect domestic industry and jobs.

- Workers in export industries benefit from trade. Moreover, all workers are consumers and benefit from the expanded market choices and lower prices that trade brings.

Key Terms

- comparative advantage

-

The concept that a certain good can be produced more efficiently than others due to a number of factors, including productive skills, climate, natural resource availability, and so forth.

- inflation

-

An increase in the general level of prices or in the cost of living.

It is asserted that trade has created jobs for foreign workers at the expense of American workers. It is more accurate to say that trade both creates and destroys jobs in the economy in line with market forces.

Economy-wide trade creates jobs in industries that have comparative advantage and destroys jobs in industries that have a comparative disadvantage. In the process, the economy’s composition of employment changes; but, according to economic theory, there is no net loss of jobs due to trade. Over the course of the last economic expansion, from 1992 to 2000, U.S. imports increased nearly 240%. Over that same period, total employment grew by 22 million jobs ,and the unemployment rate fell from 7.5% to 4.0% (the lowest unemployment rate in more than 30 years.). Foreign outsourcing by American firms, which has been the object of much recent attention, is a form of importing and also creates and destroys jobs, leaving the overall level of employment unchanged. There is no denying that with international trade there will be short-run hardship for some, but economists maintain the whole economy’s living standard is raised by such exchange. They view these adverse effects as qualitatively the same as those induced by purely domestic disruptions, such as shifting consumer demand or technological change. In that context, economists argue that easing adjustment of those harmed is economically more fruitful than protection given the net economic benefit of trade to the total economy. Many people believe that imports from countries with low wages has put downward pressure on the wages of Americans.

There is no doubt that international trade can have strong effects, good and bad, on the wages of American workers. The plight of the worker adversely affected by imports comes quickly to mind. But it is also true that workers in export industries benefit from trade. Moreover, all workers are consumers and benefit from the expanded market choices and lower prices that trade brings. Yet, concurrent with the large expansion of trade over the past 25 years, real wages (i.e., inflation adjusted wages) of American workers grew more slowly than in the earlier post-war period, and the inequality of wages between the skilled and less skilled worker rose sharply. Was trade the force behind this deteriorating wage performance? Some industries, or at least components of some industries, are vital to national security and possibly may need to be insulated from the vicissitudes of international market forces. This determination needs to be made on a case-by-case basis since the claim is made by some who do not meet national security criteria. Such criteria may also vary from case to case. It is also true that national security could be compromised by the export of certain dual-use products that, while commercial in nature, could also be used to produce products that might confer a military advantage to U.S. adversaries. Controlling such exports is clearly justified from a national security standpoint; but, it does come at the cost of lost export sales and an economic loss to the nation. Minimizing the economic welfare loss from such export controls hinges on a well- focused identification and regular re-evaluation of the subset of goods with significant national security potential that should be subject to control.

Korea International Trade Association

KITA attempts to protect South Korean producers while finding international export markets.

4.2.6: The Argument Against Barriers

Economists generally agree that trade barriers are detrimental and decrease overall economic efficiency.

Learning Objective

Argue against the imposition of trade barriers

Key Points

- Trade barriers are often criticized for the effect they have on the developing world.

- Even countries promoting free trade heavily subsidize certain industries, such as agriculture and steel.

- Most trade barriers work on the same principle: the imposition of some sort of cost on trade that raises the price of the traded products. If two or more nations repeatedly use trade barriers against each other, then a trade war results.

Key Term

- trade war

-

The practice of nations creating mutual tariffs or similar barriers to trade.

Most trade barriers work on the same principle: the imposition of some sort of cost on trade that raises the price of the traded products. If two or more nations repeatedly use trade barriers against each other, then a trade war results

Economists generally agree that trade barriers are detrimental and decrease overall economic efficiency, this can be explained by the theory of comparative advantage. In theory, free trade involves the removal of all such barriers, except perhaps those considered necessary for health or national security. In practice, however, even those countries promoting free trade heavily subsidize certain industries, such as agriculture and steel.

International trade

International trade is the exchange of goods and services across national borders. In most countries, it represents a significant part of GDP.

Trade barriers are often criticized for the effect they have on the developing world. Because rich-country players call most of the shots and set trade policies, goods, such as crops that developing countries are best at producing, still face high barriers. Trade barriers, such as taxes on food imports or subsidies for farmers in developed economies, lead to overproduction and dumping on world markets, thus lowering prices and hurting poor-country farmers. Tariffs also tend to be anti-poor, with low rates for raw commodities and high rates for labor-intensive processed goods.

If international trade is economically enriching, imposing barriers to such exchanges will prevent the nation from fully realizing the economic gains from trade and must reduce welfare. Protection of import-competing industries with tariffs, quotas, and non-tariff barriers can lead to an over-allocation of the nation’s scarce resources in the protected sectors and an under-allocation of resources in the unprotected tradeable goods industries. In the terms of the analogy of trade as a more efficient productive process used above, reducing the flow of imports will also reduce the flow of exports. Less output requires less input. Clearly, the exporting sector must lose as the protected import-competing activities gain. But, more importantly, from this perspective the overall economy that consumed the imported goods must also lose, because the more efficient production process–international trade–cannot be used to the optimal degree, and, thereby, will have generally increased the price and reduced the array of goods available to the consumer. Therefore, the ultimate economic cost of the trade barrier is not a transfer of well-being between sectors, but a permanent net loss to the whole economy arising from the barriers distortion toward the less efficient the use of the economy’s scarce resources.

4.3: International Trade Agreements and Organizations

4.3.1: The General Agreement on Tariffs and Trade (GATT)

The General Agreement on Tariffs and Trade (GATT) is a multilateral agreement regulating international trade.

Learning Objective

Outline the history of the creation of the General Agreement on Tariffs and Trade (GATT)

Key Points

- The General Agreement on Tariffs and Trade (GATT) is a multilateral agreement regulating international trade, the purpose of which is the “substantial reduction of tariffs and other trade barriers and the elimination of preferences, on a reciprocal and mutually advantageous basis”.

- The failure to create the International Trade Organization (ITO) resulted in the GATT negotiation at the UN Conference on Trade and Employment.

- GATT was in place from 1947-1993, when it was replaced by the World Trade Organization (WTO) in 1995.

- GATT text is still in effect under the WTO framework, subject to modifications.

- During GATT’s eight rounds, countries exchanged tariff concessions and reduced tariffs.

Key Terms

- multilateral

-

Involving more than one party (often used in politics to refer to negotiations, talks, or proceedings involving several nations).

- tariff

-

A system of government-imposed duties levied on imported or exported goods; a list of such duties, or the duties themselves.

The General Agreement on Tariffs and Trade (GATT) is a multilateral agreement regulating international trade. According to its preamble, its purpose is the “substantial reduction of tariffs and other trade barriers and the elimination of preferences, on a reciprocal and mutually advantageous basis. ” GATT was negotiated during the UN Conference on Trade and Employment and was the outcome of the failure of negotiating governments to create the International Trade Organization (ITO). GATT was signed in 1947 and lasted until 1993, when it was replaced by the World Trade Organization (WTO) in 1995. The original GATT text (GATT 1947) is still in effect under the WTO framework, subject to the modifications of GATT 1994.

GATT held a total of eight rounds, during which countries exchanged tariff concessions and reduced tariffs.

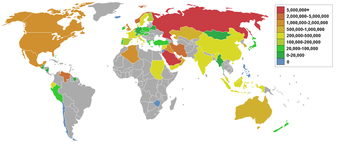

In 1993, the GATT was updated (GATT 1994) to include new obligations upon its signatories. One of the most significant changes was the creation of the WTO. The 75 existing GATT members and the European Communities became the founding members of the WTO on January 1, 1995. The other 52 GATT members rejoined the WTO in the following two years, the last being Congo in 1997. Since the founding of the WTO, 21 new non-GATT members have joined and 29 are currently negotiating membership. There are a total of 157 member countries in the WTO, with Russia and Vanuatu being new members as of 2012.

Of the original GATT members, Syria and SFR Yugoslavia (SFRY) have not rejoined the WTO. Because FR Yugoslavia (later renamed Serbia and Montenegro) is not recognized as a direct SFRY successor state, its application is considered a new (non-GATT) one. The General Council of WTO, on 4 May 2010, agreed to establish a working party to examine the request of Syria for WTO membership. The contracting parties who founded the WTO ended official agreement of the “GATT 1947” terms on 31 December 1995. Serbia and Montenegro are in the decision stage of the negotiations and are expected to become the newest members of the WTO in 2012 or in the near future.

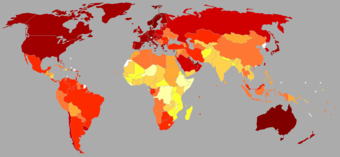

WTO Membership, 2005

GATT was replaced by the World Trade Organization (WTO) in 1995. This map shows membership in the WTO in 2005.

4.3.2: The European Union

The European Union (EU) is an economic and political union made up of 27 member states that are located primarily in Europe.

Learning Objective

Discuss the establishment of the European Union (EU) and the Euro

Key Points

- The European Union (EU) is an economic and political union made up of 27 member states that are located primarily in Europe.

- Members of the EU include Austria, Belgium, Bulgaria, Cyprus, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, and the United Kingdom.

- The EU operates through a system of supranational independent institutions and intergovernmental negotiated decisions by the member states.

- Within the Schengen Area (which includes EU and non-EU states) passport controls have been abolished.

- The creation of a single currency became an official objective of the European Economic Community (EEC) in 1969. On January 1, 2002 euro notes and coins were issued and national currencies began to phase out in the eurozone.

- The ECB is the central bank for the eurozone, and thus controls monetary policy in that area with an agenda to maintain price stability. It is at the center of the European System of Central Banks, which comprises all EU national central banks and is controlled by its General Council, consisting of the President of the ECB, who is appointed by the European Council, the Vice-President of the ECB, and the governors of the national central banks of all 27 EU member states.

Key Terms

- European Union

-

A supranational organization created in the 1950s to bring the nations of Europe into closer economic and political connection. At the beginning of 2012, 27 member nations were Austria, Belgium, Bulgaria, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, The Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, United Kingdom.

- euro

-

The currency unit of the European Monetary Union. Symbol: €

- transparency

-

Open, public; having the property that theories and practices are publicly visible, thereby reducing the chance of corruption.

Example

- The euro is designed to help build a single market by easing travel of citizens and goods, eliminating exchange rate problems, providing price transparency, creating a single financial market, stabilizing prices, maintaining low interest rates, and providing a currency used internationally and protected against shocks by the large amount of internal trade within the eurozone. It is also intended as a political symbol of integration.

The European Union

The European Union (EU) is an economic and political union or confederation of 27 member states that are located in Europe, including:

Austria, Belgium, Bulgaria, Cyprus, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, and the United Kingdom.

The EU operates through a system of supranational independent institutions and intergovernmental decisions negotiated by the member states. Important institutions of the EU include the European Commission, the Council of the European Union, the European Council, the Court of Justice of the European Union, and the European Central Bank. The European Parliament is elected every five years by EU citizens. The EU has developed a single market through a standardized system of laws that apply in all member states. Within the Schengen Area (which includes EU and non-EU states) passport controls have been abolished. EU policies aim to ensure the free movement of people, goods, services, and capital, enact legislation in justice and home affairs, and maintain common policies on trade, agriculture, fisheries, and regional development. A monetary union, the eurozone, was established in 1999, and as of January 2012, is composed of 17 member states. Through the Common Foreign and Security Policy the EU has developed a limited role in external relations and defense. Permanent diplomatic missions have been established around the world. The EU is represented at the United Nations, the WTO, the G8 and the G-20.

The Euro

The creation of a single European currency became an official objective of the European Economic Community in 1969. However, it was only with the advent of the Maastricht Treaty in 1993 that member states were legally bound to start the monetary union. In 1999 the euro was duly launched by eleven of the then fifteen member states of the EU. It remained an accounting currency until 1 January 2002, when euro notes and coins were issued and national currencies began to phase out in the eurozone, which by then consisted of twelve member states. The eurozone (constituted by the EU member states that have adopted the euro) has since grown to seventeen countries, the most recent being Estonia, which joined on 1 January 2011. All other EU member states, except Denmark and the United Kingdom, are legally bound to join the euro when the convergence criteria are met, however only a few countries have set target dates for accession. Sweden has circumvented the requirement to join the euro by not meeting the membership criteria.

The euro is designed to help build a single market by easing travel of citizens and goods, eliminating exchange rate problems, providing price transparency, creating a single financial market, stabilizing prices, maintaining low interest rates, and providing a currency used internationally and protected against shocks by the large amount of internal trade within the eurozone. It is also intended as a political symbol of integration. The euro and the monetary policies of those who have adopted it in agreement with the EU are under the control of the European Central Bank (ECB). The ECB is the central bank for the eurozone, and thus controls monetary policy in that area with an agenda to maintain price stability. It is at the center of the European System of Central Banks, which comprises all EU national central banks and is controlled by its General Council, consisting of the President of the ECB, who is appointed by the European Council, the Vice-President of the ECB, and the governors of the national central banks of all 27 EU member states. The monetary union has been shaken by the European sovereign-debt crisis since 2009.

European Union

European Union member countries

4.3.3: The North American Free Trade Agreement (NAFTA)

NAFTA is an agreement signed by Canada, Mexico, and the United States, creating a trilateral trade bloc in North America.

Learning Objective

Outline the stipulations of NAFTA

Key Points

- The North American Free Trade Agreement (NAFTA) is an agreement signed by the governments of Canada, Mexico, and the United States, creating a trilateral trade bloc in North America.

- NAFTA came into effect on January 1, 1994 and superseded the Canada – United States Free Trade Agreement.

- Within 10 years of the implementation of NAFTA, all U.S.-Mexico tariffs are to be eliminated except for some U.S. agricultural exports to Mexico which will be phased out within 15 years.

- Most U.S. – Canada trade was duty free before NAFTA.

- NAFTA also seeks to eliminate non-tariff trade barriers and to protect the intellectual property right of the products.

- When viewing the combined GDP of its members, as of 2010 NAFTA is the largest trade bloc in the world.

Key Terms

- tariff

-

A system of government-imposed duties levied on imported or exported goods; a list of such duties, or the duties themselves.

- free trade

-

International trade free from government interference, especially trade free from tariffs or duties on imports.

- trade bloc

-

A trade bloc is a type of intergovernmental agreement, often part of a regional intergovernmental organization, where regional barriers to trade, (tariffs and non-tariff barriers) are reduced or eliminated among the participating states.

The North American Free Trade Agreement (NAFTA)

The North American Free Trade Agreement (NAFTA) is an agreement signed by the governments of Canada, Mexico, and the United States, creating a trilateral trade bloc in North America. The agreement came into force on January 1, 1994. It superseded the Canada – United States Free Trade Agreement between the U.S. and Canada.

In terms of combined GDP of its members, the trade bloc is the largest in the world as of 2010. NAFTA has two supplements: the North American Agreement on Environmental Cooperation (NAAEC) and the North American Agreement on Labor Cooperation (NAALC). The goal of NAFTA was to eliminate barriers to trade and investment among the U.S., Canada, and Mexico.

The implementation of NAFTA on January 1, 1994 brought the immediate elimination of tariffs on more than one-half of Mexico’s exports to the U.S. and more than one-third of U.S. exports to Mexico. Within 10 years of the implementation of the agreement, all U.S.–Mexico tariffs would be eliminated except for some U.S. agricultural exports to Mexico that were to be phased out within 15 years. Most U.S.–Canada trade was already duty free. NAFTA also seeks to eliminate non-tariff trade barriers and to protect the intellectual property right of the products.

The agreement opened the door for open trade, ending tariffs on various goods and services, and implementing equality between Canada, America, and Mexico. NAFTA has allowed agricultural goods such as eggs, corn, and meats to be tariff-free. This allowed corporations to trade freely and import and export various goods on a North American scale .

NAFTA countries

The members of NAFTA are the U.S., Canada, and Mexico.

4.3.4: The Asia-Pacific Economic Cooperation

APEC is a forum for 21 Pacific Rim countries that seeks to promote free trade and economic cooperation throughout the Asia-Pacific region.

Learning Objective

Explain the role The Asia-Pacific Economic Cooperation (APEC ) plays in ensuring free trade

Key Points

- Asia-Pacific Economic Cooperation (APEC) is a forum for 21 Pacific Rim countries that seeks to promote free trade and economic cooperation.

- APEC was established in 1989 in response to the growing interdependence of Asia-Pacific economies and the advent of regional economic blocs.

- APEC member countries include Australia, Brunei, Canada, Chile, China, Hong Kong (Hong Kong, China), Indonesia, Japan, South Korea, Mexico, Malaysia, New Zealand, Papua New Guinea, Peru, Philippines, Russia, Singapore, Taiwan (Chinese Taipei), Thailand, United States, and Vietnam.

- During the meeting in 1994 in Bogor, Indonesia, APEC leaders adopted the Bogor Goals which aim for free and open trade and investment in the Asia-Pacific by 2010, for industrialized economies and by 2020, for developing economies.

Key Term

- bloc

-

A group of countries acting together for political or economic goals, an alliance (e.g., the eastern bloc, the western bloc, a trading bloc).

The Asia-Pacific Economic Cooperation (APEC) is a forum for 21 Pacific Rim countries (formally Member Economies) that seeks to promote free trade and economic cooperation throughout the Asia-Pacific region. Established in 1989 in response to the growing interdependence of Asia-Pacific economies and the advent of regional economic blocs (such as the European Union) in other parts of the world, APEC works to raise living standards and education levels through sustainable economic growth and to foster a sense of community and an appreciation of shared interests among Asia-Pacific countries.

Member countries are: Australia, Brunei, Canada, Chile, China, Hong Kong (Hong Kong, China), Indonesia, Japan, South Korea, Mexico, Malaysia, New Zealand, Papua New Guinea, Peru, Philippines, Russia, Singapore, Taiwan (Chinese Taipei), Thailand, United States, and Vietnam.

APEC member countries

APEC’s member countries border both the east and the west of the Pacific Ocean.

During the meeting in 1994 in Bogor, Indonesia, APEC leaders adopted the Bogor Goals that aim for free and open trade and investment in the Asia-Pacific by 2010, for industrialized economies and by 2020, for developing economies. In 1995, APEC established a business advisory body named the APEC Business Advisory Council (ABAC), composed of three business executives from each member economy. To meet the Bogor Goals, APEC carries out work in three main areas:

- Trade and investment liberalization

- Business facilitation

- Economic and technical cooperation

APEC is considering the prospects and options for a Free Trade Area of the Asia-Pacific (FTAAP), which would include all APEC member economies. Since 2006, the APEC Business Advisory Council, promoting the theory that a free trade area has the best chance of converging the member nations and ensuring stable economic growth under free trade, has lobbied for the creation of a high-level task force to study and develop a plan for a free trade area. The proposal for a FTAAP arose due to the lack of progress in the Doha round of World Trade Organization negotiations, and as a way to overcome the “spaghetti bowl” effect created by overlapping and conflicting elements of the umpteen free trade agreements. There are approximately 60 free trade agreements, with an additional 117 in the process of negotiation in Southeast Asia and the Asia-Pacific region.

4.3.5: The World Bank

The World Bank is an international financial institution that provides loans to developing countries for various programs.

Learning Objective

Explain the role played by the World Bank in reducing poverty

Key Points

- The World Bank’s official goal is the reduction of poverty.

- According to the World Bank’s Articles of Agreement, all of its decisions must be guided by a commitment to promote foreign investment, international trade, and facilitate capital investment.

- The current President of the Bank, Jim Yong Kim, is responsible for chairing the meetings of the boards of directors and for overall management of the bank.

- Traditionally, the bank president has always been a U.S. citizen nominated by the United States, the largest shareholder in the bank. The nominee is subject to confirmation by the board of executive directors, to serve for a five-year, renewable term.

- For the poorest developing countries in the world, the bank’s assistance plans are based on poverty reduction strategies.

Key Terms

- developing

-

Of a country: becoming economically more mature or advanced; becoming industrialized.

- loan

-

A sum of money or other valuables or consideration that an individual, group, or other legal entity borrows from another individual, group, or legal entity (the latter often being a financial institution) with the condition that it be returned or repaid at a later date (sometimes with interest).

- poverty

-

The quality or state of being poor or indigent; want or scarcity of means of subsistence; indigence; need.

- World Bank

-

a group of five financial organizations whose purpose is economic development and the elimination of poverty

The World Bank is an international financial institution that provides loans to developing countries for capital programs. The World Bank’s official goal is the reduction of poverty. According to the World Bank’s Articles of Agreement (as amended effective February 16,1989), all of its decisions must be guided by a commitment to promote foreign investment, international trade, and facilitate capital investment.

The World Bank differs from the World Bank Group, in that the World Bank comprises only two institutions: the International Bank for Reconstruction and Development (IBRD) and the International Development Association (IDA), whereas the former incorporates these two in addition to three more: International Finance Corporation (IFC), Multilateral Investment Guarantee Agency (MIGA), and International Centre for Settlement of Investment Disputes (ICSID). The curent President of the Bank, Jim Yong Kim, is responsible for chairing the meetings of the boards of directors and for overall management of the bank. Traditionally, the bank president has always been a U.S. citizen nominated by the United States, the largest shareholder in the bank. The nominee is subject to confirmation by the board of executive directors, to serve for a five-year, renewable term.

The International Bank for Reconstruction and Development (IBRD) has 188 member countries, while the International Development Association (IDA) has 172 members.Each member state of IBRD should be also a member of the International Monetary Fund (IMF), and only members of IBRD are allowed to join other institutions within the Bank (such as IDA).

For the poorest developing countries in the world, the bank’s assistance plans are based on poverty reduction strategies; by combining a cross-section of local groups with an extensive analysis of the country’s financial and economic situation, the World Bank develops a strategy pertaining uniquely to the country in question. The government then identifies the country’s priorities and targets for the reduction of poverty, and the World Bank aligns its aid efforts correspondingly. Forty-five countries pledged $25.1 billion in “aid for the world’s poorest countries,” aid that goes to the World Bank International Development Association (IDA) which distributes the loans to 80 poorer countries.

World Bank Headquarters

Washington, DC headquarters of the World Bank

4.3.6: The International Monetary Fund (IMF)

The IMF seeks to promote international economic cooperation, international trade, employment, and exchange rate stability.

Learning Objective

Explain how the International Monetary Fund (IMF) aids its 188 member countries

Key Points

- The International Monetary Fund (IMF) is an international organization that was created on July 22, 1944 at the Bretton Woods Conference.

- The IMF’s stated goal is to stabilize exchange rates and assist the reconstruction of the world’s international payment system after World War II.

- The IMF is run by country contributions. Money is pooled through a quota system from which countries with payment imbalances can borrow funds on a temporary basis.

- It works with developing nations to help them achieve macroeconomic stability and reduce poverty. The rationale for this is that private international capital markets function imperfectly and many countries have limited access to financial markets. Such market imperfections, together with balance of payments financing, provide the justification for official financing, without which many countries could only correct large external payment imbalances through measures with adverse effects on both national and international economic prosperity. The IMF can provide other sources of financing to countries in need that would not be available in the absence of an economic stabilization program supported by the Fund.

- Member countries of the IMF have access to information on the economic policies of all member countries, the opportunity to influence other members’ economic policies, technical assistance in banking, fiscal affairs, and exchange matters, financial support in times of payment difficulties, and increased opportunities for trade and investment. IMF conditionality is a set of policies that the IMF requires in exchange for financial resources. The IMF does not require collateral from countries for loans but rather requires the government seeking assistance to correct its macroeconomic imbalances in the form of policy reform. If the conditions are not met, the funds are withheld. Conditionality is perhaps the most controversial aspect of IMF policies.

- These loan conditions ensure that the borrowing country will be able to repay the Fund and that the country won’t attempt to solve their balance of payment problems in a way that would negatively impact the international economy. The incentive problem of moral hazard, which is the actions of economic agents maximizing their own utility to the detriment of others when they do not bear the full consequences of their actions, is mitigated through conditions rather than providing collateral; countries in need of IMF loans do not generally possess internationally valuable collateral anyway. Conditionality also reassures the IMF that the funds lent to them will be used for the purposes defined by the Articles of Agreement and provides safeguards that country will be able to rectify its macroeconomic and structural imbalances. In the judgment of the Fund, the adoption by the member of certain corrective measures or policies will allow it to repay the Fund, thereby ensuring that the same resources will be available to support other members.

- Voting power in the IMF is, like the money pool, based on a quota system. Each member has a number of “basic votes” (each member’s number of basic votes equals 5.502% of the total votes), plus one additional vote for each Special Drawing Right (SDR) of 100,000 of a member country’s quota. The Special Drawing Right is the unit of account of the IMF and represents a claim to currency. It is based on a basket of key international currencies. The basic votes generate a slight bias in favor of small countries, but the additional votes determined by SDR outweigh this bias.

- The IMF is mandated to oversee the international monetary and financial system and monitor the economic and financial policies of its 188 member countries. This activity is known as surveillance and facilitates international cooperation. Since the demise of the Bretton Woods system of fixed exchange rates in the early 1970s, surveillance has evolved largely by way of changes in procedures rather than through the adoption of new obligations. The responsibilities of the Fund changed from those of guardian to those of overseer of members’ policies.

- Some critics assume that Fund lending imposes a burden on creditor countries. However, countries receive market-related interest rates on most of their quota subscription, plus any of their own-currency subscriptions that are loaned out by the Fund, plus all of the reserve assets that they provide the Fund. Also, as of 2005 borrowing countries have had a very good track record of repaying credit extended under the Fund’s regular lending facilities with the full interest over the duration of the borrowing.

Key Terms

- collateral

-

A security or guarantee (usually an asset) pledged for the repayment of a loan if one cannot procure enough funds to repay. (Originally supplied as “accompanying” security. )

- capital market

-

The market for long-term securities, including the stock market and the bond market.

- moral hazard

-

The prospect that a party insulated from risk may behave differently from the way it would behave if it were fully exposed to the risk.

The International Monetary Fund (IMF) is an international organization that was created on July 22, 1944 at the Bretton Woods Conference and came into existence on December 27, 1945 when 29 countries signed the IMF Articles of Agreement. It originally had 45 members. The IMF’s stated goal was to stabilize exchange rates and assist the reconstruction of the world’s international payment system post-World War II. Countries contribute money to a pool through a quota system from which countries with payment imbalances can borrow funds on a temporary basis. Through this activity and others, such as surveillance of its members’ economies and policies, the IMF works to improve the economies of its member countries. The IMF describes itself as “an organization of 188 countries, working to foster global monetary cooperation, secure financial stability, facilitate international trade, promote high employment and sustainable economic growth, and reduce poverty. “

The organization’s stated objectives are to promote international economic cooperation, international trade, employment, and exchange rate stability, including by making financial resources available to member countries to meet balance of payments needs. Member countries of the IMF have access to information on the economic policies of all member countries, the opportunity to influence other members’ economic policies, technical assistance in banking, fiscal affairs, and exchange matters, financial support in times of payment difficulties, and increased opportunities for trade and investment. Voting power in the IMF is based on a quota system. Each member has a number of “basic votes” (each member’s number of basic votes equals 5.502% of the total votes), plus one additional vote for each Special Drawing Right (SDR) of 100,000 of a member country’s quota. The Special Drawing Right is the unit of account of the IMF and represents a claim to currency. It is based on a basket of key international currencies. The basic votes generate a slight bias in favor of small countries, but the additional votes determined by SDR outweigh this bias.

The IMF works to foster global growth and economic stability. It provides policy advice and financing to members in economic difficulties and also works with developing nations to help them achieve macroeconomic stability and reduce poverty. The rationale for this is that private international capital markets function imperfectly, and many countries have limited access to financial markets. Such market imperfections, together with balance of payments financing, provide the justification for official financing, without which many countries could only correct large external payment imbalances through measures with adverse effects on both national and international economic prosperity. The IMF can provide other sources of financing to countries in need that would not be available in the absence of an economic stabilization program supported by the fund.

The IMF is mandated to oversee the international monetary and financial system and monitor the economic and financial policies of its 188 member countries. This activity is known as “surveillance” and facilitates international cooperation. Since the demise of the Bretton Woods system of fixed exchange rates in the early 1970s, surveillance has evolved largely by way of changes in procedures rather than through the adoption of new obligations.The responsibilities of the fund changed from those of guardian to those of overseer of members’ policies. The fund typically analyzes the appropriateness of each member country’s economic and financial policies for achieving orderly economic growth, and assesses the consequences of these policies for other countries and for the global economy.

IMF conditionality is a set of policies or “conditions” that the IMF requires in exchange for financial resources. The IMF does not require collateral from countries for loans but rather requires the government seeking assistance to correct its macroeconomic imbalances in the form of policy reform. If the conditions are not met, the funds are withheld. Conditionality is the most controversial aspect of IMF policies. These loan conditions ensure that the borrowing country will be able to repay the fund and that the country won’t attempt to solve their balance of payment problems in a way that would negatively impact the international economy. The incentive problem of moral hazard, which is the actions of economic agents maximizing their own utility to the detriment of others when they do not bear the full consequences of their actions, is mitigated through conditions rather than providing collateral; countries in need of IMF loans do not generally possess internationally valuable collateral anyway. Conditionality also reassures the IMF that the funds lent to them will be used for the purposes defined by the Articles of Agreement and provides safeguards that country will be able to rectify its macroeconomic and structural imbalances. In the judgment of the fund, the adoption by the member of certain corrective measures or policies will allow it to repay the fund, thereby ensuring that the same resources will be available to support other members.

IMF Headquarters

Washington, DC headquarters of the IMF

4.3.7: Common Markets

A common market is the first stage towards a single market and may be limited initially to a free trade area.

Learning Objective

Explain the history of the European Economic Community (EEC)

Key Points

- A common market is the first stage towards a single market and may be limited initially to a free trade area, with relatively free movement of capital and of services. However, it is not to a stage where the remaining trade barriers have been eliminated.

- The European Economic Community (EEC) (also known as the Common Market in the English-speaking world and sometimes referred to as the European Community even before it was renamed as such in 1993) was an international organization created by the 1957 Treaty of Rome.

- The main aim of the EEC, as stated in its preamble, was to “preserve peace and liberty and to lay the foundations of an ever closer union among the peoples of Europe”.

Key Term

- free trade

-

International trade free from government interference, especially trade free from tariffs or duties on imports.

Example

- The European Economic Community was the first example of a both common and single market, but it was an economic union since it had additionally a customs union. The European Economic Community (EEC) was an international organization created by the 1957 Treaty of Rome. Its aim was to bring about economic integration, including a common market, among its six founding members: Belgium, France, Germany, Italy, Luxembourg and the Netherlands. Upon the entry into force of the Maastricht Treaty in 1993, the EEC was renamed the European Community (EC) to reflect that it covered a wider range of policy. This was also when the three European Communities, including the EC, were collectively made to constitute the first of the three pillars of the European Union (EU). For the customs union, the treaty provided for a 10% reduction in custom duties and up to 20% of global import quotas. Progress on the customs union proceeded much faster than the twelve years planned.

A common market is a first stage towards a single market and may be limited initially to a free trade area with relatively free movement of capital and of services, but not so advanced in reduction of the rest of the trade barriers.

The European Economic Community (EEC) (also known as the Common Market in the English-speaking world and sometimes referred to as the European Community even before it was renamed as such in 1993) was an international organization created by the 1957 Treaty of Rome. Its aim was to bring about economic integration, including a common market, among its six founding members: Belgium, France, Germany, Italy, Luxembourg, and the Netherlands.

It gained a common set of institutions along with the European Coal and Steel Community (ECSC) and the European Atomic Energy Community (EURATOM) as one of the European Communities under the 1965 Merger Treaty (Treaty of Brussels).

Upon the entry into force of the Maastricht Treaty in 1993, the EEC was renamed the European Community (EC) to reflect that it covered a wider range of policy. This was also when the three European Communities, including the EC, were collectively made to constitute the first of the three pillars of the European Union (EU), which the treaty also founded. The EC existed in this form until it was abolished by the 2009 Treaty of Lisbon, which merged the EU’s former pillars and provided that the EU would “replace and succeed the European Community. ” The main aim of the EEC, as stated in its preamble, was to “preserve peace and liberty and to lay the foundations of an ever closer union among the peoples of Europe. ” Calling for balanced economic growth, this was to be accomplished through:

- The establishment of a customs union with a common external tariff

- Common policies for agriculture, transport, and trade

- Enlargement of the EEC to the rest of Europe

For the customs union, the treaty provided for a 10% reduction in custom duties and up to 20% of global import quotas. Progress on the customs union proceeded much faster than the 12 years planned. However, France faced some setbacks due to its war with Algeria.

The six states that founded the EEC and the other two communities were known as the “inner six” (the “outer seven” were those countries who formed the European Free Trade Association). The six were France, West Germany, Italy, and the three Benelux countries: Belgium, the Netherlands, and Luxembourg. The first enlargement was in 1973, with the accession of Denmark, Ireland, and the United Kingdom. Greece, Spain, and Portugal joined in the 1980s. Following the creation of the EU in 1993, it has enlarged to include an additional 15 countries by 2007.

There were three political institutions that held the executive and legislative power of the EEC, plus one judicial institution and a fifth body created in 1975. These institutions (except for the auditors) were created in 1957 by the EEC but from 1967 on, they applied to all three communities. The council represents governments, the Parliament represents citizens, and the commission represents the European interest.

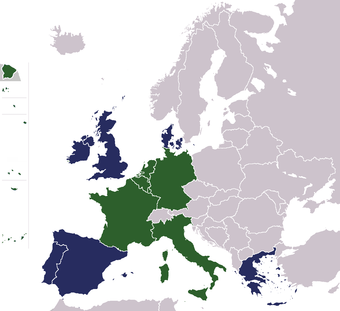

European Economic Community

Original member states (blue) and later members (green)

4.3.8: The Export-Import Bank of the United States

The Export-Import Bank of the United States (Ex-Im Bank) is the official export credit agency of the United States federal government.

Learning Objective

Explain the purpose of the Export-Import Bank of the United States (Ex-Im Bank)

Key Points

- The mission of the Ex-Im Bank is to create and sustain U.S. jobs by financing sales of U.S. exports to international buyers.

- Ex-Im Bank provides financing for transactions that would otherwise not take place because commercial lenders are either unable or unwilling to accept the political or commercial risks inherent in the deal.

- The Export-Import Bank of the United States focuses much of its energy and resources on providing support to U.S. small businesses for export of American-made products.

- Export Credit Insurance from Export-Import Bank of the United States provides insurance policies to U.S. companies and banks to mitigate risks of non-collection from foreign buyers and borrowers.

- The Working Capital Guarantee program provides loan guarantees to banks willing to lend to exporting companies.

Key Terms

- risk

-

To incur risk [of something].

- guarantee

-

To assume responsibility for a debt.

- credit agency

-

A credit rating agency (CRA) is a company that assigns credit ratings for issuers of certain types of debt obligations as well as the debt instruments themselves. In some cases, the servicers of the underlying debt are also given ratings.

Example

- The Ex-Im Bank provides two types of loans: direct loans to foreign buyers of American exports and intermediary loans to responsible parties, such as foreign government lending agencies that re-lend to foreign buyers of capital goods and related services (for example, a maintenance contract for a jet passenger plane).

The Export-Import Bank of the United States (Ex-Im Bank) is the official export credit agency of the United States federal government. It was established in 1934 by an executive order and made an independent agency in the Executive branch by Congress in 1945. Its purpose is to finance and insure foreign purchases of United States goods for customers unable or unwilling to accept credit risk.

The mission of the Ex-Im Bank is to create and sustain U.S. jobs by financing sales of U.S. exports to international buyers. Ex-Im Bank is the principal government agency responsible for aiding the export of American goods and services through a variety of loan, guarantee, and insurance programs. Generally, its programs are available to any American export firm regardless of size. The Bank is chartered as a government corporation by the Congress of the United States; it was last chartered for a five year term in 2006. Its Charter spells out the Bank’s authorities and limitations. Among them is the principle that Ex-Im Bank does not compete with private sector lenders, but rather provides financing for transactions that would otherwise not take place because commercial lenders are either unable or unwilling to accept the political or commercial risks inherent in the deal.

Export-Import Bank of the United States

Seal of the Export-Import Bank of the United States.

Ex-Im Bank provides the following services:

- The Export-Import Bank of the United States focuses much of its energy and resources on providing support to small American businesses for export of American-made products

- Export Credit Insurance provides insurance policies to U.S. companies and banks to mitigate risks of non-collection from foreign buyers and borrowers.

- The Working Capital Guarantee program provides loan guarantees to banks willing to lend to exporting companies.

- Two types of loans: direct loans to foreign buyers of American exports and intermediary loans to responsible parties, such as foreign government lending agencies that re-lend to foreign buyers of capital goods and related services (for example, a maintenance contract for a jet passenger plane).

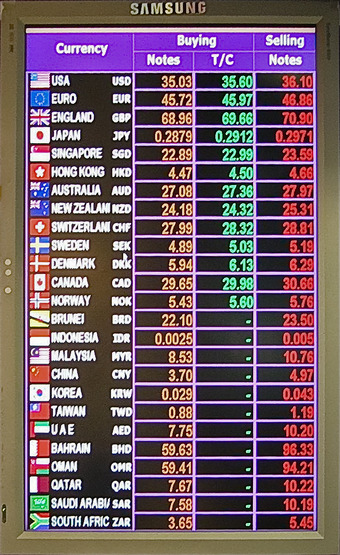

4.4: The Money of International Business

4.4.1: Exchange Rates

The price of one country’s currency in units of another country’s currency is known as a foreign currency exchange rate.

Learning Objective

Summarize how exchange rates operate

Key Points

- An exchange rate between two currencies is the rate at which one currency will be exchanged for another.

- Currency may be free-floating, pegged or fixed, or a hybrid.

- A currency will tend to become more valuable whenever demand for it is greater than the available supply.

- Increased demand for a currency can be due to either an increased transaction demand for money or an increased speculative demand for money.

Key Terms

- exchange rate

-

The amount of one currency that a person or institution defines as equivalent to another currency when either buying or selling it at any particular moment.

- fixed exchange rate

-

Sometimes called a pegged exchange rate, a type of exchange rate regime wherein a currency’s value is matched to the value of another single currency or to a basket of other currencies, or to another measure of value, such as gold.

- floating exchange rate

-

A floating or fluctuating exchange rate is a type of exchange rate regime wherein a currency’s value is allowed to fluctuate according to the foreign exchange market.

Example