Keynesian theory posits that aggregate demand will not always meet the supply produced.

Learning Objective

Explain the main tenets of Keynesian economics

Key Points

John Maynard Keynes published a book in 1936 called The General Theory of Employment, Interest, and Money, laying the groundwork for his legacy of the Keynesian Theory of Economics.

Keynes positioned his argument in contrast to this idea, stating that markets are imperfect and will not always self correct.

Keynes believed that wage reductions in recessions and excessive savings were potential threats to an economy.

Keynesian theory expects fiscal policy to offset business cycles (employ counter-cyclical strategies).

Key Terms

Keynesian

Of or pertaining to an economic theory based on the ideas of John Maynard Keynes, as put forward in his book The General Theory of Employment, Interest, and Money.

monetary policy

The process of controlling the supply of money in an economy, often conducted by central banks.

fiscal policy

Government policy that attempts to influence the direction of the economy through changes in government spending or taxes.

Historical Background

John Maynard Keynes published a book in 1936 called The General Theory of Employment, Interest, and Money, laying the groundwork for his legacy of the Keynesian Theory of Economics. It was an interesting time for economic speculation considering the dramatic adverse effect of the Great Depression . Keynes’s concepts played a role in public economic policy under Roosevelt as well as during World War II, becoming the dominant perspective in Europe following the war.

John Maynard Keynes

John Maynard Keynes came to fame after publishing his economic theories during the Great Depression.

At the time, the primary school of economic thought was that of the classical economists (which is still a popular school of thought today). The central tenet of the classical argument says that supply can always create demand, and that surpluses will result in price reductions to the point of consumption. Put simply, people have infinite needs and the market will self-correct to the aggregate demands and available resources. This implies a hands-of public policy where markets are capable of taking care of themselves.

Keynes positioned his argument in contrast to this idea, stating that markets are imperfect and will not always self correct. Keynes theorized that natural inefficiencies in the market will see goods that are not met with demand. This wasted capital can result in market losses, unemployment, and market inefficiency (this was called ‘general glut’ in the classical model, when aggregate demand does not meet supply). Keynes insisted that markets do need moderate governmental intervention through fiscal policy (government investment in infrastructure) and monetary policy (interest rates).

Main Tenets

With this overview in mind, Keynesian Theory generally observes the following concepts:

Unemployment:Under the classical model, unemployment is often attributed to high and rigid real wages. Keynes argues there is more complexity than that, specifically that societies are highly resistant to wage cuts and furthermore that reducing wages would pose a great threat to an economy. Specifically, cutting wages reduces spending and may result in a downwards spiral.

Excessive Saving:Keynes’s concept here is somewhat complicated, but in short Keynes notes excessive saving as a threat and prospective cause of economic decline. This is because excessive saving leads to reduced investment and reduced spending, which drives down demand and the potential for consumption. This can be another spiraling issue, as money not being exchanged is actively reducing prospective employment, revenues, and future investments.

Fiscal Policy:The key concept in fiscal policy for Keynes is ‘counter-cyclical’ fiscal policy, which is the expectation that governments can reduce the negative effects of the natural business cycle. This is, generally, achieved through deficit spending in recessions and suppression of inflation during boom times. Simply put, the government should try to curb the extremes of economic fluctuation through informed fiscal policy.

The Multiplier Effect: This idea has in many ways already been implied in the atom, but inversely. Consider the unemployment and excessive savings problems, and how they stand to lead to spiraling decline. The other side of that coin is that positive economic situations can spiral upwards. Take for example a government investment in transportation, putting money in the pockets of various individuals who build trains and tracks. These individuals will spend that extra capital, putting money in the hands of other business (and this will continue). This is called the multiplier effect.

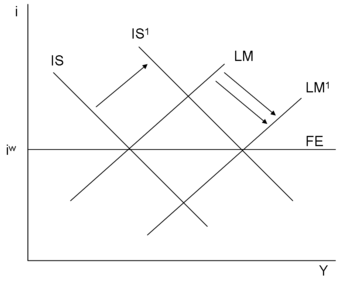

IS-LM : While the IS-LM Model is a complicated byproduct of Keynesian economics, it can be summarized as the relationship between interest rates (y-axis) and the real economic output (x-axis). This is done through analyzing the invest-saving relationship (IS) in contrast to the liquidity preference and money supply relationship (LM), generating an equilibrium where certain interest rates and outputs will be generated.

While Keynesian Theory has been expounded upon significantly over the years, the important takeaway here is that aggregate demand (and thus the amount of supply consumed) is not a perfect system. Instead, demand is affected by various external forces that can create an inefficient market which will in turn affect employment, production, and inflation.

IS-LM Model

In this figure, the IS (Interest – Saving) curve is shifted outward in a way that raises both interest rates (i) and the ‘real’ economy (Y). The implication is that interest rates affect investment levels, and that these investment levels in turn affect the overall economy.

25.1.2: Monetarist

Monetarism focuses on the macroeconomic effects of the supply of money and the role of central banking on an economic system.

Learning Objective

Explain the main tenets of Monetarism

Key Points

Clark Warburton, in 1945, has been identified as the first thinker to draft an empirically sound argument in favor of monetarism. This was taken more mainstream by Milton Friedman in 1956.

More money in the system results in higher spending and vice verse. This would theoretically provide some control over aggregate demand.

Historical implementation of monetarism demonstrated some correlation with control over inflation rates and increased economic performance. This could have been a result of other factors however.

The Austrian school of economic thought perceives monetarism as somewhat narrow-minded, not effectively taking into account the subjectivity involved in valuing capital.

Due to the globalization of the economy, monetarism may have a negative impact on external economies. This is particularly true of the U.S., whose capital is an international standard.

Key Terms

gold standard

A monetary system where the value of circulating money is linked to the value of gold.

Monetarism

The doctrine that economic systems are controlled by variations in the supply of money.

Background

In the rise of monetarism as an ideology, two specific economists were critical contributors. Clark Warburton, in 1945, has been identified as the first thinker to draft an empirically sound argument in favor of monetarism. This was taken more mainstream by Milton Friedman in 1956 in a restatement of the quantity theory of money. The basic premise these two economists were putting forward is that the supply of money and the role of central banking play a critical role in macroeconomics.

The generation of this theory takes into account a combination of Keynesian monetary perspectives and Friedman’s pursuit of price stability. Keynes postulated a demand-driven model for currency; a perspective on printed money that was not beholden to the ‘gold standard’ (or basing economic value off of rare metal). Instead, the amount of money in a given environment should be determined by monetary rules. Friedman originally put forward the idea of a ‘k-percent rule,’ which weighed a variety of economic indicators to determine the appropriate money supply.

Evidence

Theoretically, the idea is actually quite straight-forward. When the money supply is expanded, individuals will be induced to higher spending. In turn, when the money supply retracted, individuals would limit their budgetary spending accordingly. This would theoretically provide some control over aggregate demand (which is one of the primary areas of disagreement between Keynesian and classical economists).

Monetarism began to deviate more from Keynesian economics however in the 70’s and 80’s, as active implementation and historical reflection began to generate more evidence for the monetarist view. In 1979 for example, Jimmy Carter appointed Paul Volcker as Chief of the Federal Reserve, who in turn utilized the monetarist perspective to control inflation. He eventually created a price stability, providing evidence that the theory was sound. In addition, Milton Friedman and Ann Schwartz analyzed the Great Depression in the context of monetarism as well, identifying a shortage of the money supply as a critical component of the recession.

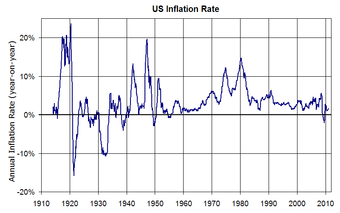

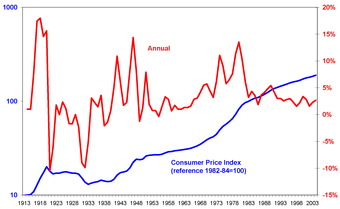

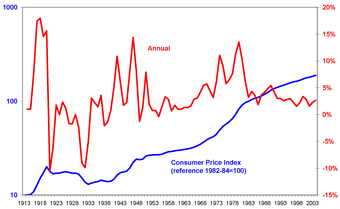

The 1980s were an interesting transitional period for this perspective, as early in the decade (1980-1983) monetary policies controlling capital were attributed to substantial reductions in inflation (14% to 3%)(see ). However, unemployment and the rise of the use of credit are quoted as two alternatives to money supply control being the primary influence of the boom that followed 1983.

U.S. Inflation Rates

The inflation rates over time in the U.S. represent some of the evidence put forward by monetarist economists, stating that governmental control of the money supply allows for some control over inflation.

Counter Arguments

As these counter arguments in the 1980s began to arise, critics of monetarism became more mainstream. Of the current monetarism critics, the Austrian school of thought is likely the most well-known. The Austrian school of economic thought perceives monetarism as somewhat narrow-minded, not effectively taking into account the subjectivity involved in valuing capital. That is to say that monetarism seems to assume an objective value of capital in an economy, and the subsequent implications on the supply and demand.

Other criticisms revolve around international investment, trade liberalization, and central bank policy. This can be summarized as the effects of globalization, and the interdependence of markets (and consequently currencies). To manipulate money supply there will inherently be effects on other currencies as a result of relativity. This is particularly important in regards to the U.S. currency, which is considered a standard in international markets. Controlling supply and altering value may have effects on a variety of internal economic variables, but it will also have unintended consequences on external variables.

25.1.3: Austrian

Austrian economic thought is about methodological individualism, or the idea that people will act in meaningful ways which can be analyzed.

Learning Objective

Explain the main tenets of Austrian economics

Key Points

The Austrian school of economics is one of the oldest economic perspectives, originating in the 19th century in Vienna.

Austrian economics is attributed for the identification of opportunity cost, capital and interest, inflation, business cycles and the organizing power of markets.

Austrian economists do not often place much weight on concepts such as econometrics, experimental economics, and aggregate macroeconomic analysis. In this sense, the Austrian school of thought is something of an outsider relative to other perspectives (i.e. classical, Keynesian, etc. ).

Paul Krugman criticized Austrian economics as lacking explicit models of analysis, or essentially a lack of clarity in their approach. This results in inadvertent blind spots.

Key Terms

Opportunity cost

The cost of any activity measured in terms of the value of the next best alternative forgone (that is not chosen).

time value of money

The time value of money is the principle that a certain currency amount of money today has a different buying power (value) than the same currency amount of money in the future.

Background

The Austrian school of economics originated in the 19th century in Vienna, Austria. While there were a variety of famous economists attributed to the early foundations and later expansions of the Austrian economic perspective, Carl Menger, Friedrich von Weiser, and Eugen von Bohm-Bawerk are widely recognized as critical early pioneers. The general perspective of Austrian economic thought is methodological individualism, or the recognition that people will act in meaningful ways which can be analyzed for trends.

Central Tenets

The Austrian school of thought provided enormous value to the economic climate, both as a foundation for future economics and as a deliberate counterpoint to more quantitative analysis. Of the most important ideologies, the following central tenets are:

Opportunity Cost: This is a concept you are likely already familiar with, and one of the most important ideas in all of business and economics. Essentially, the price of a good must also incorporate the value sacrificed of the next best alternative. Basically each choice a consumer or business makes intrinsically has the cost of not being able to make an alternative choice.

Capital and Interest: Largely in response to Karl Marx’s labor theories, Austrian economist Bohm-Bawerk identified the building blocks of interest rates and profit are supply and demand alongside time preference. In short, present consumption is more valuable than future consumption (the time value of money).

Inflation: The idea that prices and wages must rise as a result of increased money supply is inflation (note: this is different that price inflation). Simply put, more money in the system without a higher demand for that money will drive down the relative value of each dollar.

Business Cycles:The Austrian business cycle theory (ABCT) is the simple observation that the issuance of credit (by banks) creates economic fluctuations that tend to be cyclical (see ). In simple terms, banks will lend out money at rates lower than the risk in which that money will be used. So when businesses fail more often than they succeed, thus losing interest as opposed to accruing it, will struggle to repay their debts. When the banks call in those debts the business cannot pay, creating negative business cycles.

The Organizing Power of Markets: The idea of this concept is that no one person knows what the appropriate price of a good should be. Instead, markets naturally generate incentives to identify optimal price points. This negates the ideas of socialism common at the time, as communist systems will be unable to identify the appropriate exchange value of each good.

As you can see from the above points, this school of economics is largely about making qualitative observations of the markets. These observations are absolutely critical in understanding the theoretical landscape, but difficult to enact in practice.

Criticisms

Austrian economists are often criticized for ignoring arithmetic or statistical ways to measure and analyze economics. Indeed, Austrian economists do not often place much weight on concepts such as econometrics, experimental economics, and aggregate macroeconomic analysis. In this sense, the Austrian school of thought is something of an outsider relative to other perspectives (i.e. classical, Keynesian, etc.).

Paul Krugman criticized Austrian economics as lacking explicit models of analysis, or essentially a lack of clarity in their approach. This results in inadvertent blind spots. This is a sensible criticism in many ways, as the fundamental idea behind this economic theory is that it is driven by individuals and individuals are not always rational (indeed, they are quite often irrational). As a result of this, Austrian economics often rests on the integration of social sciences (psychology, sociology, etc.) to explain preferences and consumer behavior, which is often counter-intuitive. As a result, it is very difficult to accurately measure and provide tangible proof of the efficacy of Austrian models.

25.1.4: Alternative Views

Neoclassical and neo-Keynesian ideas can be coupled and referred to as the neoclassical synthesis, combining alternative views in economics.

Learning Objective

Summarize neoclassical and Neo-Keynesian economics

Key Points

The history of different economic schools of thought have consistently generated evolving theories of economics as new data and new perspectives are taken into consideration.

The neoclassical perspective in conjunction with Keynesian ideas is referred to as the neoclassical synthesis, which is largely considered the ‘mainstream’ economic perspective.

A critical difference between classical and neoclassical perspectives is the introduction of marginalism. Marginalism notes that economic participants make decisions based on marginal utility or margins.

Neo-Keynesian economics is the formalization and coordination of Keynes’s writings by a number of other economists (most notably John Hicks, Franco Modigliani and Paul Samuelson).

The important to understand that these economic perspectives add value to one another and the overall efficacy of all economic theory.

Key Terms

static

Unchanging; that cannot or does not change.

stagflation

Inflation accompanied by stagnant growth, unemployment or recession.

Background

The history of different economic schools of thought have consistently generated evolving theories of economics as new data and new perspectives are taken into consideration. The two most well-known schools, classical economics and Keynesian economics, have been adapting to incorporate new information and ideas from one another as well as lesser known schools of economics (Chicago, Austrian, etc.). These different perspectives have motivated economists to generate the neoclassical and neo-Keynesian perspectives. The neoclassical perspective, in conjunction with Keynesian ideas, is referred to as the neoclassical synthesis, which is largely considered the ‘mainstream’ economic perspective.

Neoclassical

In approaching Neoclassical economics, it is most important to keep in mind the following three principles:

People have rational preferences in the context of options or outcomes that can be identified and associated with a given value (usually monetary). In short, people make smart choices regarding how they spend their money.

Individuals maximize utility and firms maximize profit. People will try to get the most from their money while corporations will try to invest their time and assets to capture the highest margin.

People act independently based upon comprehensive and relevant information. People are influenced by rational forces (mostly information and logic), and will make the best personal purchasing decisions based upon this.

A brief timeline of classical to neoclassical perspectives would begin with thought processes put forward by Adam Smith and David Ricardo (alongside many others). The basic idea is that aggregate demand will adjust to supply, and that value theory and distribution will reflect this rational, cost of production model. The next phase was the observation that consumer goods demonstrated a relative value based on utility, which could deviate from consumer to consumer. The final phase, and most central to the advent of the neoclassical perspective, is the introduction of marginalism. Marginalism notes that economic participants make decisions based on marginal utility or margins. For example, a company hiring a new employee will not think of the fixed value of that employee, but instead the marginal value of adding that employee (usually in regards to profitability).

Neo-Keynesian

Neo-Keynesian economics is often confused with ‘New Keynesian’ economics (which attempts to provide microeconomic foundation to Keynesian views, particularly in light of stagflation in the 1970s). Neo-Keynesian economics is actually the formalization and coordination of Keynes’s writings by a number of other economists (most notably John Hicks, Franco Modigliani, and Paul Samuelson). Much of the conceptual value is captured in the previous atoms on Keynesian views, but the substantial value of a few neo-Keynesian ideas is worth reiterating:

IS/LM Model: This model was put forward by John Hicks in order to capture the inherent relationship between investment and savings (IS) relative to liquidity and the overall money supply (LM) (see ). The implications of this graph pertain to the static representation of monetary policy and the effects on an economic system.

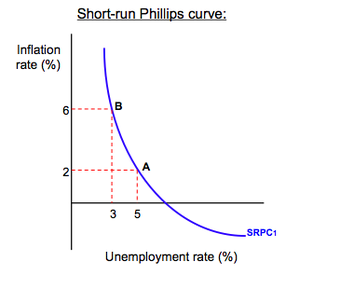

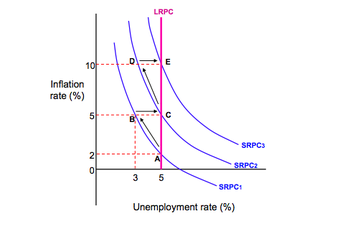

Phillips Curve: Another important model following Keynes’s publications is the Phillips Curve, put forward by William Phillips in 1958. The idea here was also largely Keynesian, revolving around the relationship between inflation and unemployment (see ).This implies a trade off between inflation rates and the creation of employment, which governments could consider in policy making. Stagflation (economic stagnation and inflation simultaneously) created issues with this however, necessitating New Keynesian ideas (as discussed briefly above).

Synthesis

When learning about these economic perspectives, it is important to understand the value they add to one another and the overall efficacy of all economic theory. Economists are often the product of multiple schools of thought, and don’t fit neatly into one school or another.

24.1.1: Defining Aggregate Expenditure: Components and Comparison to GDP

Aggregate expenditure is the current value of all the finished goods and services in the economy.

Learning Objective

Define aggregate expenditure

Key Points

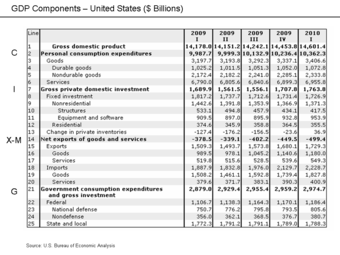

The aggregate expenditure is the sum of all the expenditures undertaken in the economy by the factors during a specific time period. The equation is: AE = C + I + G + NX.

The aggregate expenditure determines the total amount that firms and households plan to spend on goods and services at each level of income.

The aggregate expenditure is one of the methods that is used to calculate the total sum of all the economic activities in an economy, also known as the gross domestic product (GDP).

When there is excess supply over the expenditure, there is a reduction in either the prices or the quantity of the output which reduces the total output (GDP) of the economy.

When there is an excess of expenditure over supply, there is excess demand which leads to an increase in prices or output (higher GDP).

Key Terms

aggregate

A mass, assemblage, or sum of particulars; something consisting of elements but considered as a whole.

expenditure

Act of expending or paying out.

gross domestic product

A measure of the economic production of a particular territory in financial capital terms over a specific time period.

Aggregate Expenditure

In economics, aggregate expenditure is the current value of all the finished goods and services in the economy. It is the sum of all the expenditures undertaken in the economy by the factors during a specific time period. The equation for aggregate expenditure is: AE = C + I + G + NX.

Written out the equation is: aggregate expenditure equals the sum of the household consumption (C), investments (I), government spending (G), and net exports (NX).

Consumption (C): The household consumption over a period of time.

Investment (I): The amount of expenditure towards the capital goods.

Government expenditure (G): The amount of spending by federal, state, and local governments. Government expenditure can include infrastructure or transfers which increase the total expenditure in the economy.

Net exports (NX): Total exports minus the total imports.

The aggregate expenditure determines the total amount that firms and households plan to spend on goods and services at each level of income.

Comparison to GDP

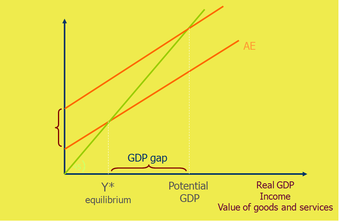

The aggregate expenditure is one of the methods that is used to calculate the total sum of all the economic activities in an economy, also known as the gross domestic product (GDP). The gross domestic product is important because it measures the growth of the economy. The GDP is calculated using the Aggregate Expenditures Model .

Aggregate Expenditure

This graph shows the aggregate expenditure model. It is used to determine and graph the real GPD, potential GDP, and point of equilibrium. A shift in supply or demand impacts the GDP.

An economy is at equilibrium when aggregate expenditure is equal to the aggregate supply (production) in the economy. The economy is not in a constant state of equilibrium. Instead, the aggregate expenditure and aggregate supply adjust each other toward equilibrium.

When there is excess supply over the expenditure, there is a reduction in either the prices or the quantity of the output which reduces the total output (GDP) of the economy.

In contrast, when there is an excess of expenditure over supply, there is excess demand which leads to an increase in prices or output (higher GDP). A rise in the aggregate expenditure pushes the economy towards a higher equilibrium and a higher potential of the GDP.

24.1.2: Aggregate Expenditure at Economic Equilibrium

An economy is said to be at equilibrium when aggregate expenditure is equal to the aggregate supply (production) in the economy.

Learning Objective

Identify the assumptions fundamental to classical economics in regards to aggregate expenditure at economic equilibrium

Key Points

In economics, aggregate expenditure is the current value (price) of all the finished goods and services in the economy. The equation for aggregate expenditure is AE = C+ I + G + NX.

In the aggregate expenditure model, equilibrium is the point where the aggregate supply and aggregate expenditure curve intersect.

The classical aggregate expenditure model is: AE = C + I.

Classical economics states that the factor payments made during the production process create enough income in the economy to create a demand for the products that were produced.

Key Terms

aggregate

A mass, assemblage, or sum of particulars; something consisting of elements but considered as a whole.

expenditure

Act of expending or paying out.

equilibrium

The condition of a system in which competing influences are balanced, resulting in no net change.

Aggregate Expenditure

In economics, aggregate expenditure is the current value (price) of all the finished goods and services in the economy. The equation for aggregate expenditure is AE = C+ I + G + NX.

Written out in full, the equation reads: aggregate expenditure = household consumption (C) + investments (I) + government spending (G) + net exports (NX).

Aggregate expenditure is a method that is used to calculate the total value of economic activities, also referred to as the gross domestic product (GDP). The GDP of an economy is calculated using the aggregate expenditure model.

Economic Equilibrium

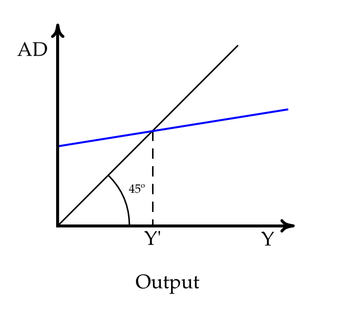

An economy is said to be at equilibrium when aggregate expenditure is equal to the aggregate supply (production) in the economy. The economy is constantly shifting between excess supply (inventory) and excess demand. As a result, the economy is always moving towards an equilibrium between the aggregate expenditure and aggregate supply. On the aggregate expenditure model, equilibrium is the point where the aggregate supply and aggregate expenditure curve intersect. An increase in the expenditure by consumption (C) or investment (I) causes the aggregate expenditure to rise which pushes the economy towards a higher equilibrium .

Aggregate Expenditure – Equilibrium

In this graph, equilibrium is reached when the total demand (AD) equals the total amount of output (Y). The equilibrium point is where the blue line intersects with the black line.

Classical Economics – Aggregate Expenditure

Classical economists believed in Say’s law, which states that supply creates its own demand. This idea stems from the belief that wages, prices, and interest rage were all flexible. Classical economics states that the factor payments (wage and rental payments) made during the production process create enough income in the economy to create a demand for the products that were produced. This belief is parallel to Adam Smith’s invisible hand – markets achieve equilibrium through the market forces that impact economic activity.

The classical aggregate expenditure model is: AE = C + I .

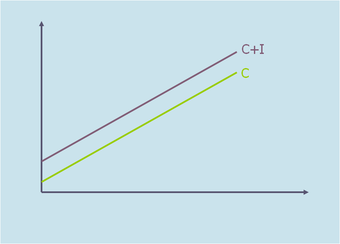

Classical Aggregate Expenditure

This graph shows the classical aggregate expenditure where C is consumption expenditure and I is aggregate investment. The aggregate expenditure is the aggregate consumption plus the planned investment (AE = C + I).

The aggregate expenditure equals the aggregate consumption plus planned investment. Classical economics assumes that the economy works on a full-employment equilibrium, which is not always true. In reality, many economists argue that the economy operates at an under-employment equilibrium.

24.1.3: Graphing Equilibrium

An economy is said to be at equilibrium when the aggregate expenditure is equal to the aggregate supply (production) in the economy.

Learning Objective

Demonstrate how aggregate demand and aggregate supply determine output and price level by using the AD-AS model

Key Points

Aggregate supply (AS) is the total supply of goods and services that firms in an economy plan on selling during a specific time period.

Aggregate demand (AD) is the total demand for final goods and services in the economy at a given time and price level.

Aggregate expenditure is the current value of all the finished goods and services in the economy. The equation for aggregate expenditure is: AE = C + I + G + NX.

The AD-AS model is used to graph the aggregate expenditure at the point of equilibrium.

Key Terms

equilibrium

The condition of a system in which competing influences are balanced, resulting in no net change.

aggregate demand

The the total demand for final goods and services in the economy at a given time and price level.

aggregate supply

The total supply of goods and services that firms in a national economy plan on selling during a specific time period.

Aggregate Supply and Aggregate Demand

In economics, the aggregate supply (AS) is the total supply of goods and services that firms in an economy produce during a specific time period. It represents the total amount of goods and services that firms are willing to sell at a given price level. The aggregate supply curve is graphed as a backwards L-shape in the short-run and vertical in the long-run.

Aggregate demand (AD) is the total demand for final goods and services in the economy at a given time and price level. It shows the amounts of goods and services that will be purchased at all the possible price levels. When aggregate demand increases its graph shifts to the right. It shifts to the left when it decreases which shows a fall in output and prices.

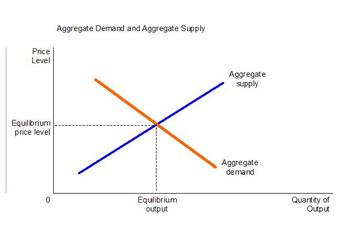

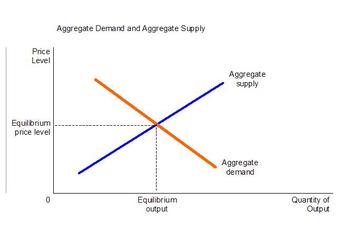

The aggregate supply and aggregate demand determine the output and price for goods and services. The AD-AS model is used to graph the aggregate expenditure and the point of equilibrium .

AD-AS Model

This graph shows the AD-AS model where P is the average price level and Y* is the aggregate quantity demanded. The model is used to show how increases in aggregate demand leads to increases in prices (inflation) and in output.

Aggregate Expenditure

Aggregate expenditure is the current value of all the finished goods and services in the economy. The equation for aggregate expenditure is: AE = C + I + G + NX.

The aggregate expenditure equals the sum of the household consumption (C), investments (I), government spending (G), and net exports (NX).

Graphing Equilibrium

The AD-AS model is used to graph the aggregate expenditure at the point of equilibrium. The AD-AS model includes price changes. An economy is said to be at equilibrium when the aggregate expenditure is equal to the aggregate supply (production) in the economy. It is important to note that the economy does not stay in a state of equilibrium. The aggregate expenditure and aggregate supply adjust each other towards equilibrium. When there is excess supply over expenditure, there is a reduction in the prices or the quantity or output. When there is an excess of expenditure over supply, then there is excess demand which leads to an increase in prices out output. In an effort to adjust and reach equilibrium, the economy constantly shifts between excess supply and excess demand. This shift is graphed using the AD-AS model which determines the output and price for the good or service.

24.1.4: The Multiplier Effect

When the fiscal multiplier exceeds one, the resulting impact on the national income is called the multiplier effect.

Learning Objective

Explain the fiscal multiplier effect

Key Points

In economics, the fiscal multiplier is the ratio of change in the national income in relation to the change in government spending that causes it.

The multiplier is influenced by an incremental amount of spending that leads to higher consumption spending, increased income, and then even more consumption. As a result, the overall national income is greater than the initial incremental amount of spending.

The multiplier effect is a tool that is used by governments to attempt to stimulate aggregate demand in times of recession or economic uncertainty.

The multiplier effect is criticized because it can create over crowding and an increase in the number of negative externalities.

Key Terms

fiscal multiplier

The ratio of a change in national income to the change in government spending that causes it.

multiplier effect

A factor of proportionality that measures how much an endogenous variable changes in response to a change in some exogenous variable.

The Fiscal Multiplier and the Multiplier Effect

In economics, the fiscal multiplier is the ratio of change in the national income in relation to the change in government spending that causes it (not to be confused with the monetary multiplier). National income can change as a direct result in a change in spending whether it is private investment spending, consumer spending, government spending, or foreign export spending. When the fiscal multiplier exceeds one, the resulting impact on the national income is called the multiplier effect.

Cause of the Multiplier Effect

The multiplier is influenced by an incremental amount of spending that leads to higher consumption spending, increased income, and then even more consumption. As a result, the overall national income is greater than the initial incremental amount of spending. Simply put, an initial shift in aggregate demand may cause a change in aggregate output (as well as the aggregate income it creates) that is a multiplier of the initial change.

Use of the Multiplier Effect

The multiplier effect is a tool that is used by governments to attempt to stimulate aggregate demand in times of recession or economic uncertainty . The government invests money in order to create more jobs, which in turn will generate more spending to stimulate the economy. The goal is that the net increase in disposable income will be greater than the original investment.

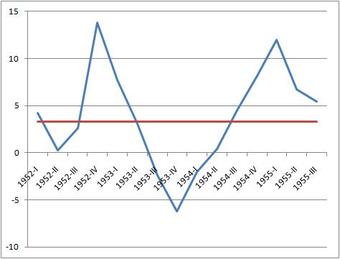

1953 U.S. Recession

This graph shows the economic recession that occurred in the U.S. in 1953. During recessions, the government can use the multiplier effect in order to stimulate the economy.

Criticisms

Although the multiplier effect usually measures values of one, there have been cases where multipliers of less than one are measured. This suggests that types of government spending can crowd out private investment or consumer spending that would have taken place without the government spending. Crowding out can occur because the initial increase in spending can cause an increase in the interest rates or the price level.

It has been argued that when a government relies heavily on fiscal multipliers, externalities such as environmental degradation, unsustainable resource depletion, and social consequences can be neglected. Over reliance on fiscal multipliers can cause increased government spending on activities that create negative externalities (pollution, climate change, and resource depletion) instead of positive externalities (increased educational standards, social cohesion, public health, etc.).

24.2: Introducing Aggregate Demand and Aggregate Supply

24.2.1: Explaining Fluctuations in Output

In the short run, output fluctuates with shifts in either aggregate supply or aggregate demand; in the long run, only aggregate supply affects output.

Learning Objective

Differentiate between short-run and long-run effects of nominal fluctuations

Key Points

In the short run, output is determined by both the aggregate supply and aggregate demand within an economy. Anything that causes labor, capital, or efficiency to go up or down results in fluctuations in economic output.

Aggregate supply and aggregate demand are graphed together to determine equilibrium. The equilibrium is the point where supply and demand meet.

According to Hume, in the short-run, and increase in the money supply will lead to an increase in production.

According to Hume, in the long-run, an increase in the money supply will do nothing.

Key Terms

economic output

The productivity of a country or region measured by the value of goods and services produced.

nominal

Without adjustment to remove the effects of inflation (in contrast to real).

Economic Output

In economics, output is the quantity of goods and services produced in a given time period. The level of output is determined by both the aggregate supply and aggregate demand within an economy. National output is what makes a country rich, not large amounts of money. For this reason, understanding the fluctuations in economic output is critical for long term growth. There are a series of factors that influence fluctuations in economic output including increases in growth and inputs in factors of production. Anything that causes labor, capital, or efficiency to go up or down results in fluctuations in economic output.

Aggregate Supply and Aggregate Demand

Aggregate supply is the total amount of goods and services that firms are willing to sell at a given price in an economy. The aggregate demand is the total amounts of goods and services that will be purchased at all possible price levels.

In a standard AS-AD model, the output (Y) is the x-axis and price (P) is the y-axis. Aggregate supply and aggregate demand are graphed together to determine equilibrium. The equilibrium is the point where supply and demand meet to determine the output of a good or service.

Short-run vs. Long-run Fluctuations

Supply and demand may fluctuate for a number of reasons, and this in turn may affect the level of output. There are noticeable differences between short-run and long-run fluctuations in output.

Over the short-run, an outward shift in the aggregate supply curve would result in increased output and lower prices. An outward shift in the aggregate demand curve would also increase output and raise prices. Short-run nominal fluctuations result in a change in the output level . In the short-run an increase in money will increase production due to a shift in the aggregate supply. More goods are produced because the output is increased and more goods are bought because of the lower prices.

AS-AD Model

This AS-AD model shows how the aggregate supply and aggregate demand are graphed to show economic output. The AD curve shifts to the right which increases output and price.

In the long-run, the aggregate supply curve and aggregate demand curve are only affected by capital, labor, and technology. Everything in the economy is assumed to be optimal. The aggregate supply curve is vertical which reflects economists’ belief that changes in aggregate demand only temporarily change the economy’s total output. In the long-run an increase in money will do nothing for output, but it will increase prices.

24.2.2: Classical Theory

Classical theory, the first modern school of economic thought, reoriented economics from individual interests to national interests.

Learning Objective

Identify the assumptions fundamental to classical economics

Key Points

When classical theory emerged, society was undergoing many changes. The primary economic question involved how a society could be organized around a system in which every individual sought his own monetary gain.

Classical economics focuses on the growth in the wealth of nations and promotes policies that create national economic expansion.

Classical theory assumptions include the beliefs that markets self-regulate, prices are flexible for goods and wages, supply creates its own demand, and there is equality between savings and investments.

Key Term

self-regulating

Describing something capable of controlling itself.

Classical Theory

Classical theory was the first modern school of economic thought. It began in 1776 and ended around 1870 with the beginning of neoclassical economics. Notable classical economists include Adam Smith, Jean-Baptiste Say, David Ricardo, Thomas Malthus, and John Stuart Mill . During the period in which classical theory emerged, society was undergoing many changes. The primary economic question involved how a society could be organized around a system in which every individual sought his own monetary gain. It was not possible for a society to grow as a unit unless its members were committed to working together. Classical theory reoriented economics away from individual interests to national interests. Classical economics focuses on the growth in the wealth of nations and promotes policies that create national expansion. During this time period, theorists developed the theory of value or price which allowed for further analysis of markets and wealth. It analyzed and explained the price of goods and services in addition to the exchange value.

Adam Smith

Adam Smith was one of the individuals who helped establish classical economic theory.

Classical Theory Assumptions

Classical theory was developed according to specific economic assumptions:

Self-regulating markets: classical theorists believed that free markets regulate themselves when they are free of any intervention. Adam Smith referred to the market’s ability to self-regulate as the “invisible hand” because markets move towards their natural equilibrium without outside intervention.

Flexible prices: classical economics assumes that prices are flexible for goods and wages. They also assumed that money only affects price and wage levels.

Supply creates its own demand: based on Say’s Law, classical theorists believed that supply creates its own demand. Production will generate an income enough to purchase all of the output produced. Classical economics assumes that there will be a net saving or spending of cash or financial instruments.

Equality of savings and investment: classical theory assumes that flexible interest rates will always maintain equilibrium.

Calculating real GDP: classical theorists determined that the real GDP can be calculated without knowing the money supply or inflation rate.

Real and Nominal Variables: classical economists stated that real and nominal variables can be analyzed separately.

24.2.3: Keynesian Theory

Keynesian economics states that in the short-run, economic output is substantially influenced by aggregate demand.

Learning Objective

Differentiate “Chicago School” or “Austrian School” economists from “Keynesian School” economists

Key Points

Keynesian theory was first introduced by British economist John Maynard Keynes in his book The General Theory of Employment, Interest, and Money, which was published in 1936 during the Great Depression.

Keynesian theorists believe that aggregate demand is influenced by a series of factors and responds unexpectedly. Shifts in aggregate demand impact production, employment, and inflation in the economy.

Unemployment is the result of structural inadequacies within the economic system. It is not a product of laziness as believed previously.

During a recession the economy may not return naturally to full employment. The government must step in and utilize government spending to stimulate economic growth. A lack of investment in goods and services causes the economy to operate below its potential output and growth rate.

Overcoming an economic depression required economic stimulus, which could be achieved by cutting interest rates and increasing the level of government investment.

Key Term

Keynesian Economics

A school of thought that is characterized by a belief in active government intervention in an economy and the use of monetary policy to promote growth and stability.

Keynesian Theory

In economics, the Keynesian theory was first introduced by British economist John Maynard Keynes in his book The General Theory of Employment, Interest, and Money which was published in 1936 during the Great Depression . Keynesian economics states that in the short-run, especially during recessions, economic output is substantially influenced by aggregate demand (the total spending in the economy). According to the Keynesian theory, aggregate demand does not necessarily equal the productive capacity of the economy. Keynesian theorists believe that aggregate demand is influenced by a series of factors and responds unexpectedly. The shift in aggregate demand impacts production, employment, and inflation in the economy.

John Maynard Keynes

John Maynard Keynes introduced Keynesian theory in his book, The General Theory of Employment, Interest, and Money.

Economic Thought

At the time that Keynesian theory was developed, mainstream economic thought believed that the economy existed in a state of general equilibrium. The belief was that the economy naturally consumes whatever it produces because the act of producing creates enough income in the economy for that consumption to take place.

Keynesian theory has certain characteristic beliefs:

Unemployment is the result of structural inadequacies within the economic system. It is not a product of laziness as believed previously.

During a recession, the economy may not return naturally to full employment. The government must step in and utilize government spending to stimulate economic growth. A lack of investment in goods and services causes the economy to operate below its potential output and growth rate.

An active stabilization policy is needed to reduce the amplitude of the business cycle. Keynesian economists believed that aggregate demand for goods and services not meeting the supply was one of the most serious economic problems.

Excessive saving, saving beyond investment, is a serious problem that encouraged recession and even depression.

Cutting wages will not cure a recession.

Overcoming an economic depression requires economic stimulus, which could be achieved by cutting interest rates and increasing the level of government investment.

Schools of Economic Thought

It is important to understand the stances of the various school of economic thought. Although the beliefs of each school vary, all of the schools of economic thought have contributed to economic theory is some way.

The Keynesian School of economic thought emphasized the need for government intervention in order to stabilize and stimulate the economy during a recession or depression. In contrast, the Chicago School of economic thought focused price theory, rational expectations, and free market policies with little government intervention. The Austrian School of economic thought focused on the belief that all economic phenomena are caused by the subjective choices of individuals. Unlike other schools, the Austrian school focused on individual actions instead of society as a whole.

24.3: Aggregate Demand

24.3.1: Introducing Aggregate Demand

Aggregate demand (AD) is defined as the total demand for final goods and services in a given economy at a specific time.

Learning Objective

Define Aggregate Demand

Key Points

To put it simply, AD is the sum of all demand in an economy. It is often called the effective demand or aggregate expenditure (AE), and is the demand of all gross domestic product (GDP).

In summary, the calculation of aggregate demand can be represented as follows: AD = Consumption + Investment + Government spending + Net export (exports – imports).

Many societies have increasingly adopted debt and credit as an integral part of their economic system. This has justified the incorporation of debt (also called the credit impulse) into the larger framework of aggregate demand.

There is some loss of accuracy in combining such a diverse array of economic inputs when calculating aggregate demand.

Key Terms

expenditure

The act of incurring a cost or pay out.

aggregate demand

In macroeconomics, aggregate demand (AD) is the total demand for final goods and services in the economy at a given time and price level.

Aggregate demand (AD) is defined as the total demand for final goods and services in a given economy at a specific time. Unlike other illustrations of demand, it is inclusive of all amounts of the product or service purchased at any possible price level. Simply put, AD is the sum of all demand in an economy. It is often called the effective demand or aggregate expenditure (AE), and is the demand of all gross domestic product (GDP).

Demand Sources

Consumption (C): This is the simplest and largest component of aggregate demand (usually 40-60% of all demand), and is often what is intuitively thought of as demand. Consumption is just the amount of consumer spending executed in an economy. Taxes play a role in this exchange as well (i.e. sales tax).

Investment (I):Investment is a relatively large portion of demand as well, and is referred to as Gross Domestic Fixed Capital Formation. This is the money spent by firms on capital investment (new machinery, factories, stocks, etc.). Investment equates to about 10% of GDP in most economies.

Government Spending (G):This is referred to as General Government Final Consumption, and is the expenditure by the government. This can include welfare, social services, education, military, etc. Fiscal policy is the way in which governments can alter this spending to drive economic change.

Net Export (NX):This can be put simply as the sale of goods to foreign countries subtracted by the purchase of goods from other countries (X-M). Trade surpluses and deficits can occur based on whether or not exports or imports are higher.

In summary, the calculation of aggregate demand can be represented as follows: AD = C + I + G + (X-M). The full sum of all demand in an economy takes into account each of these factors in a quantitative way. This curve is illustrated in the figure .

Aggregate Demand and Supply

This graph demonstrates the basic relationship between aggregate demand and aggregate supply. The aggregate demand curve is derived via the consumption, investment, government spending, and net export.

The Role of Debt

Many societies have increasingly adopted debt and credit as an integral part of their economic system. This has justified the incorporation of debt (also called the credit impulse) into the larger framework of aggregate demand. From a quantitative perspective this is simply expressed as: Spending = Income + Net Increase in Debt. Spending capital prior to the receipt of capital is an important consideration at both the consumer level and the government level (deficit spending).

The Aggregation Problem

There are some limitations to the aggregation perspective, generally summarized as the aggregation problem. The difficulty arises in treating all consumer preferences (and thus their respective demands) as homogeneous and continuous. As the numbers of consumers, the tastes of consumers and the distribution levels of incomes will alter, so too will the demand curve. This can create inaccurate assumptions in AD inputs. Simply, there is some loss of accuracy in combining such a diverse array of economic inputs.

24.3.2: The Slope of the Aggregate Demand Curve

Due to Pigou’s Wealth Effect, the Keynes’ Interest Rate Effect, and the Mundell-Fleming Exchange Rate Effect, the AD curve slopes downward.

Learning Objective

Explain the factors that influence the slope of the aggregate demand curve

Key Points

Pigou’s Wealth Effect, the Keynes’ Interest Rate Effect, and the Mundell-Fleming Exchange Rate Effect are all theoretical inputs that reaffirm a downwards slope for aggregate demand (AD).

The critical takeaway from Keynes’s perspective on the slope of the aggregate demand curve is that interest rates affect expenditures more than they affect savings. As a result, insufficient AD is not sustainable in a given system.

The simplest way to put to wealth effect is that an increase in spending will denote an increase in wealth.

Robert Mundell and Marcus Fleming noted that incorporating the nominal exchange rate into the mix makes it impossible to maintain free capital movement, a fixed exchange rate and independent monetary policy.

While these varying effects make the concept of aggregate demand slopes seem somewhat complicated, the most important thing to keep in mind is that people will be demanding more goods when they are cheaper.

Key Term

liquidity trap

Injections of cash into the private banking system by a central bank fail to lower interest rates and stimulate economic growth.

Aggregate demand (AD) is the total demand for all goods within a given market at a given time, or the summation of demand curves within a system. Understanding the basic graphical representation of this curve is useful in grasping the implications of AD on an economic system, as well as the distinct effects which drive it. As a result of Keynes’ interest rate effect, Pigou’s wealth effect, and the Mundell-Fleming exchange rate effect, the AD curve is downward sloping.

Keynes’ Interest Rate Effect

The critical point from Keynes’s perspective on the slope of the aggregate demand curve is that interest rates affect expenditures more than they affect savings. If prices fall, a given amount of money will increase in value. This will drive up interest rates and investments. It is important to note that insufficient demand in a market will not go on forever.

In understanding this fully, it is useful to look at an IS-LM graph (see ). There are only two times when the Keynes observation on the interest rate effect will be inaccurate, and that is if the IS (investment savings) curve were to be vertical or if the LM (liquidity preference money supply) curve were to be horizontal. This makes sense if you think about it, it would basically equate to a liquidity trap. A vertical IS curve or a horizontal LM curve would essentially negate the way in which interest rates could affect aggregate demand.

IS-LM Model

The IS-LM model takes investments and savings and compares that to liquidity and the overall money supply. It is highly useful in understanding macroeconomics from a Keynesian perspective. Interest rates (i) are on the vertical axis, and output (y) is on the horizontal axis.

Pigou’s Wealth Effect

In the context of the above discussion on Keynes, Pigou’s Wealth Effect underlines the fact that liquidity traps are not sustainable. The simplest way to explain the Wealth Effect is that an increase in spending will denote an increase in wealth. In many ways, what Pigou is putting forward is the idea that downwards spiral on the IS-LM model , as predicted by Keynes due to deflation, will be counterbalanced by an increase in real wages and thus an increase in expenditure. In other words, a decrease in employment and prices will eventually see higher purchasing power and an increase in spending, creating wealth.

Mundell-Fleming Exchange Rate Effect

Perhaps the most complex of the three inputs underlined in deriving aggregate demand is the Mundell-Fleming Exchange Rate Effect. Just like the previous two, this builds off of the IS-LM model in a way that discusses it in the context of an open economy (as opposed to a closed system). It essentially takes into account a new factor (in addition to interest rates and outputs, as the traditional IS-LM model incorporates). This new factor is the exchange rates, as the name implies. Robert Mundell and Marcus Fleming noted that incorporating the nominal exchange rate into the mix makes it impossible to maintain free capital movement, a fixed exchange rate and independent monetary policy. This is sometimes referred to as the ‘impossible trinity,’ implying that trade-offs must be made. This concept is illustrated fairly well in this figure , where ‘FE’ is fixed expenditure.

Mundell-Fleming Fixed Exchange Rate Illustration

An increase in government spending forces the monetary authority to supply the market with local currency to keep the exchange rate unchanged. Shown here is the case of perfect capital mobility, in which the BoP curve (or, as denoted here, the FE curve) is horizontal.

Conclusion

While these varying effects make the concept of aggregate demand slopes seem somewhat complicated, the most important thing to keep in mind is that people will be demanding more goods when they are cheaper. The analysis of interest rates displayed above, through the wealth effect in particular, offsets the negative spiral that could occur as a result of deflation and decreased employment. These effects also play a crucial role in understanding the way in which the larger and more complex environment, including investments and fiscal and monetary policy, will retain this downwards slope.

24.3.3: Reasons for and Consequences of Shifts in the Aggregate Demand Curve

An increase in any of the four inputs into AD will result in higher real output or an increase in prices.

Learning Objective

Describe exogenous events that can shift the aggregate demand curve

Key Points

There are four basic inputs to consider in calculating AD: consumption (C), investment (I), government spending (G) and net exports (NX, which is exports (X) – imports (I)).

There are a variety of direct and indirect consequences in AD shifts. For the purpose of this discussion, it is most important to keep in mind changes in output and price.

As the system moves closer to the highest potential output (optimal utilization of resources, or Y*), scarcity will naturally cause prices to increase more than the overall output in a system.

As the system moves closer to the highest potential output (or optimal utilization of resources, or Y*), scarcity will naturally see the prices increases more so than the overall output in a system.

Key Term

exogenous

Received from outside a group

Aggregate demand (AD) is the summation of all demand within a given economy at a given time.

Inputs

There are four inputs to consider in calculating AD (and deriving the graphical curve which represents it): consumption (C), investment (I), government spending (G), and net exports (NX, which is exports (X) – imports (I)). Changes in these inputs will have some influence on the AD curve. For example, an increase in total expenditures will result in a shift rightwards, while a decrease in expenditure will result in a shift to the left.

Aggregate Demand Curves

Two specific AD representations are useful to consider:

Keynesian Cross: The Keynesian Cross is a simple illustration of the relationship between aggregate demand and desired total spending (linear at 45 degrees). The intersecting AD line will generally have an upwards slope, under the assumption that increased national output should result in increased disposable income.

Aggregate Demand/Aggregate Supply Model (AD/AS):The x-axis represents the overall output, while the y-axis represents the price level. The aggregate quantity demanded (Y = C + I + G + NX) is calculated at every given aggregate average price level.

Exogenous Effects

There are a variety of direct and indirect consequences to AD shifts. For the purpose of this discussion, the key consequences to keep in mind are changes in output and price. Below are some of the driving forces that will shift aggregate demand to the right:

An exogenous increase in consumer spending;

An exogenous increase in investment spending on physical capital;

An exogenous increase in intended inventory investment;

An exogenous increase in government spending on goods and services;

An exogenous increase in transfer payments from the government to the people;

An exogenous decrease in taxes levied;

An exogenous increase in purchases of the country’s exports by people in other countries; and

An exogenous decrease in imports from other countries.

Short-term Implications

As noted above, any increase in the overall AD will result in an outwards (right-ward) shift of the AD curve. (Conversely, a decrease in aggregate demand will cause a leftward shift of the AD curve. ) This means that an increase in any of the four inputs to AD will result in a higher quantity of real output or an increase in prices across the board (this is also known as inflation). However, different levels of economic activity will result in different combinations of output and price increases.

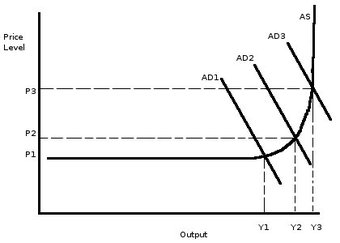

is useful for understanding the distribution between price increases and output increases that will result in a given economy when AD increases. To put simply, the lower the utilization of available resources in a system, the more an increase in AD will result in higher output and thus higher employment and GDP growth. However, as the system evolves and aligns itself closer to the highest potential output (optimal utilization of resources or Y*), scarcity will naturally cause the prices to increase more than the overall output in a system. This is somewhat intuitive economically when scarcity and utilization are taken into account. The more difficult it is to generate a supply increase the more likely a shift in AD will drive up prices.

Aggregate Supply/Aggregate Demand

This graph illustrates the relationship between price and output within a given economic system in the context of aggregate demand and supply.

24.4: Aggregate Supply

24.4.1: Introducing Aggregate Supply

Aggregate supply is the total supply of goods and services that firms in a national economy plan to sell during a specific time period.

Learning Objective

Define Aggregate Supply

Key Points

Aggregate supply is the relationship between the price level and the production of the economy.

In the short-run, the aggregate supply is graphed as an upward sloping curve.

The short-run aggregate supply equation is: Y = Y* + α(P-Pe). In the equation, Y is the production of the economy, Y* is the natural level of production of the economy, the coefficient α is always greater than 0, P is the price level, and Pe is the expected price level from consumers.

In the long-run, the aggregate supply is graphed vertically on the supply curve.

The equation used to determine the long-run aggregate supply is: Y = Y*. In the equation, Y is the production of the economy and Y* is the natural level of production of the economy.

Key Terms

output

Production; quantity produced, created, or completed.

factor of production

A resource employed to produce goods and services, such as labor, land, and capital.

Aggregate Supply

In economics, aggregate supply is the total supply of goods and services that firms in a national economy plan to sell during a specific time period. It is the total amount of goods and services that the firms are willing to sell at a given price level in the economy. Aggregate supply is the relationship between the price level and the production of the economy .

Aggregate Supply

Aggregate supply is the total quantity of goods and services supplied at a given price. Its intersection with aggregate demand determines the equilibrium quantity supplied and price.

Short-run Aggregate Supply

In the short-run, the aggregate supply is graphed as an upward sloping curve. The equation used to determine the short-run aggregate supply is: Y = Y* + α(P-Pe). In the equation, Y is the production of the economy, Y* is the natural level of production of the economy, the coefficient α is always greater than 0, P is the price level, and Pe is the expected price level from consumers.

The short-run aggregate supply curve is upward sloping because the quantity supplied increases when the price rises. In the short-run, firms have one fixed factor of production (usually capital). When the curve shifts outward the output and real GDP increase at a given price. As a result, there is a positive correlation between the price level and output, which is shown on the short-run aggregate supply curve.

Long-run Aggregate Supply

In the long-run, the aggregate supply is graphed vertically on the supply curve. The equation used to determine the long-run aggregate supply is: Y = Y*. In the equation, Y is the production of the economy and Y* is the natural level of production of the economy.

The long-run aggregate supply curve is vertical which reflects economists’ beliefs that changes in the aggregate demand only temporarily change the economy’s total output. In the long-run, only capital, labor, and technology affect aggregate supply because everything in the economy is assumed to be used optimally. The long-run aggregate supply curve is static because it is the slowest aggregate supply curve.

24.4.2: The Slope of the Short-Run Aggregate Supply Curve

In the short-run, the aggregate supply curve is upward sloping.

Learning Objective

Summarize the characteristics of short-run aggregate supply

Key Points

The AS curve is drawn using a nominal variable, such as the nominal wage rate. In the short-run, the nominal wage rate is fixed. As a result, an increasing price indicates higher profits that justify the expansion of output.

The AS curve increases because some nominal input prices are fixed in the short-run and as output rises, more production processes encounter bottlenecks.

In the short-run, the production can be increased without much diminishing returns. The average price level does not have to rise much in order to justify increased production. In this case, the AS curve is flat.

When demand is high, there are few production processes that have unemployed fixed outputs. Any increase in demand production causes the prices to increase which results in a steep or vertical AS curve.

Key Terms

supply

The amount of some product that producers are willing and able to sell at a given price, all other factors being held constant.

aggregate

A mass, assemblage, or sum of particulars; something consisting of elements but considered as a whole.

Aggregate Supply

Aggregate supply is the total supply of goods and services that firms in a national economy plan to sell during a specific period of time. It is the total amount of goods and services that firms are willing to sell at a given price level.

Short-run Aggregate Supply Curve

In the short-run, the aggregate supply curve is upward sloping. There are two main reasons why the quantity supplied increases as the price rises:

The AS curve is drawn using a nominal variable, such as the nominal wage rate. In the short-run, the nominal wage rate is fixed. As a result, an increasing price indicates higher profits that justify the expansion of output.

An alternate model explains that the AS curve increases because some nominal input prices are fixed in the short-run and as output rises, more production processes encounter bottlenecks. At low levels of demand, large numbers of production processes do not make full use of their fixed capital equipment. As a result, production can be increased without much diminishing returns. The average price level does not have to rise much in order to justify increased production. In this case, the AS curve is flat. Likewise, when demand is high, there are few production processes that have unemployed fixed outputs. Any increase in demand production causes the prices to increase which results in a steep or vertical AS curve.

Short-run Aggregate Supply Equation

The equation used to calculate the short-run aggregate supply is: Y = Y* + α(P-Pe). In the equation, Y is the production of the economy, Y* is the natural level of production, coefficient is always positive, P is the price level, and Pe is the expected price level.

In the short-run, firms possess fixed factors of production, including prices, wages, and capital. It is possible for the short-run supply curve to shift outward as a result of an increase in output and real GDP at a given price . As a result, the short-run aggregate supply curve shows the correlation between the price level and output.

Aggregate Supply Curve

This graph shows the aggregate supply curve. In the short-run the aggregate supply curve is upward sloping. When the curve shifts outward, it is due to an increase in output and real GDP.

24.4.3: The Slope of the Long-Run Aggregate Supply Curve

The long-run aggregate supply curve is perfectly vertical; changes in aggregate demand only cause a temporary change in total output.

Learning Objective

Assess factors that influence the shape and movement of the long run aggregate supply curve

Key Points

The long-run is a planning and implementation phase. It is the conceptual time period in which there are no fixed factors of production.

In the long-run, only capital, labor, and technology affect the aggregate supply curve because at this point everything in the economy is assumed to be used optimally.

Aggregate supply is usually inadequate to supply ample opportunity. Often, this is fixed capital equipment. The AS curve is drawn given some nominal variable, such as the nominal wage rate.

In the long run, the nominal wage rate varies with economic conditions (high unemployment leads to falling nominal wages — and vice-versa).

The equation used to calculate the long-run aggregate supply is: Y = Y*. In the equation, Y is the level of economic production and Y* is the natural level of production.

Key Term

long-run

The conceptual time period in which there are no fixed factors of production.

Aggregate Supply

In economics, aggregate supply is defined as the total supply of goods and services that firms in a national economy are willing to sell at a given price level.

Long-run in Economics

The long-run is the conceptual time period in which there are no fixed factors of production; all factors can be changed. In the long-run, firms change supply levels in response to expected economic profits or losses.

Long-run Aggregate Supply Curve

In the long-run, only capital, labor, and technology affect the aggregate supply curve because at this point everything in the economy is assumed to be used optimally. The long-run aggregate supply curve is static because it shifts the slowest of the three ranges of the aggregate supply curve. The long-run aggregate supply curve is perfectly vertical, which reflects economists’ belief that the changes in aggregate demand only cause a temporary change in an economy’s total output . In the long-run, there is exactly one quantity that will be supplied.

Aggregate Supply

This graph shows the aggregate supply curve. In the long-run the aggregate supply curve is perfectly vertical, reflecting economists’ belief that changes in aggregate demand only cause a temporary change in an economy’s total output.

The long-run aggregate supply curve can be shifted, when the factors of production change in quantity. For example, if there is an increase in the number of available workers or labor hours in the long run, the aggregate supply curve will shift outward (it is assumed the labor market is always in equilibrium and everyone in the workforce is employed). Similarly, changes in technology can shift the curve by changing the potential output from the same amount of inputs in the long-term.

For the short-run aggregate supply, the quantity supplied increases as the price rises. The AS curve is drawn given some nominal variable, such as the nominal wage rate. In the short run, the nominal wage rate is taken as fixed. Therefore, rising P implies higher profits that justify expansion of output. However, in the long run, the nominal wage rate varies with economic conditions (high unemployment leads to falling nominal wages — and vice-versa).

The equation used to calculate the long-run aggregate supply is: Y = Y*. In the equation, Y is the level of economic production and Y* is the natural level of production.

24.4.4: Moving from Short-Run to Long-Run

In the short-run, the price level of the economy is sticky or fixed; in the long-run, the price level for the economy is completely flexible.

Learning Objective

Recognize the role of capital in the shape and movement of the short-run and long-run aggregate supply curve

Key Points

When capital increases, the aggregate supply curve will shift to the right, prices will drop, and the quantity of the good or service will increase.

The short-run aggregate supply curve is an upward slope. The short-run is when all production occurs in real time.

The long-run curve is perfectly vertical, which reflects economists’ belief that changes in aggregate demand only temporarily change an economy’s total output. The long-run is a planning and implementation stage.

Aggregate supply moves from short-run to long-run by considering some equilibrium that is the same for both short and long-run when analyzing supply and demand. That state of equilibrium is then compared to the new short-run and long-run equilibrium state from a change that disturbs equilibrium.

Key Term

capital

Already-produced durable goods available for use as a factor of production, such as steam shovels (equipment) and office buildings (structures).

In economics, the short-run is the period when general price level, contractual wages, and expectations do not fully adjust. In contrast, the long-run is the period when the previously mentioned variables adjust fully to the state of the economy.

Aggregate Supply

Aggregate supply is the total amount of goods and services that firms are willing to sell at a given price level.

When capital increases, the aggregate supply curve will shift to the right, prices will drop, and the quantity of the good or service will increase.

Short-run Aggregate Supply

During the short-run, firms possess one fixed factor of production (usually capital). It is possible for the curve to shift outward in the short-run, which results in increased output and real GDP at a given price. In the short-run, there is a positive relationship between the price level and the output . The short-run aggregate supply curve is an upward slope. The short-run is when all production occurs in real time.

Aggregate Supply

This graph shows the relationship between aggregate supply and aggregate demand in the short-run. The curve is upward sloping and shows a positive correlation between the price level and output.

Long-run Aggregate Supply

In the long-run only capital, labor, and technology impact the aggregate supply curve because at this point everything in the economy is assumed to be used optimally. The long-run supply curve is static and shifts the slowest of all three ranges of the supply curve. The long-run curve is perfectly vertical, which reflects economists’ belief that changes in aggregate demand only temporarily change an economy’s total output. The long-run is a planning and implementation stage.

Moving from Short-run to Long-run

In the short-run, the price level of the economy is sticky or fixed depending on changes in aggregate supply. Also, capital is not fully mobile between sectors.

In the long-run, the price level for the economy is completely flexible in regards to shifts in aggregate supply. There is also full mobility of labor and capital between sectors of the economy.

The aggregate supply moves from short-run to long-run when enough time passes such that no factors are fixed. That state of equilibrium is then compared to the new short-run and long-run equilibrium state if there is a change that disturbs equilibrium.

24.4.5: Reasons for and Consequences of Shifts in the Short-Run Aggregate Supply Curve

The short-run aggregate supply shifts in relation to changes in price level and production.

Learning Objective

Identify common reasons for shifts in the short-run aggregate supply curve, Explain the consequences of shifts in the short-run aggregate supply curve

Key Points

In the short-run, the aggregate supply curve is upward sloping because some nominal input prices are fixed and as the output rises, more production processes experience bottlenecks.

At low levels of demand, production can be increased without diminishing returns and the average price level does not rise.

When the demand is high, few production processes have unemployed fixed inputs. Any increase in demand and production increases the prices.